As 2022 comes to a close, let’s hit on the Top 10 things that made the (grain & oilseed) world go round these past 12 months.

Before we get to the Top 10, here are my two favorite pics of the kids from this past year:

Tripp (aka Buford T. Justice) at Halloween:

Genevieve turned three earlier this month and continues to carry that pair of goggles EVERYWHERE (i.e. was wearing them around the living room last night sort of thing):

#10 | 2022’s Winners & Losers

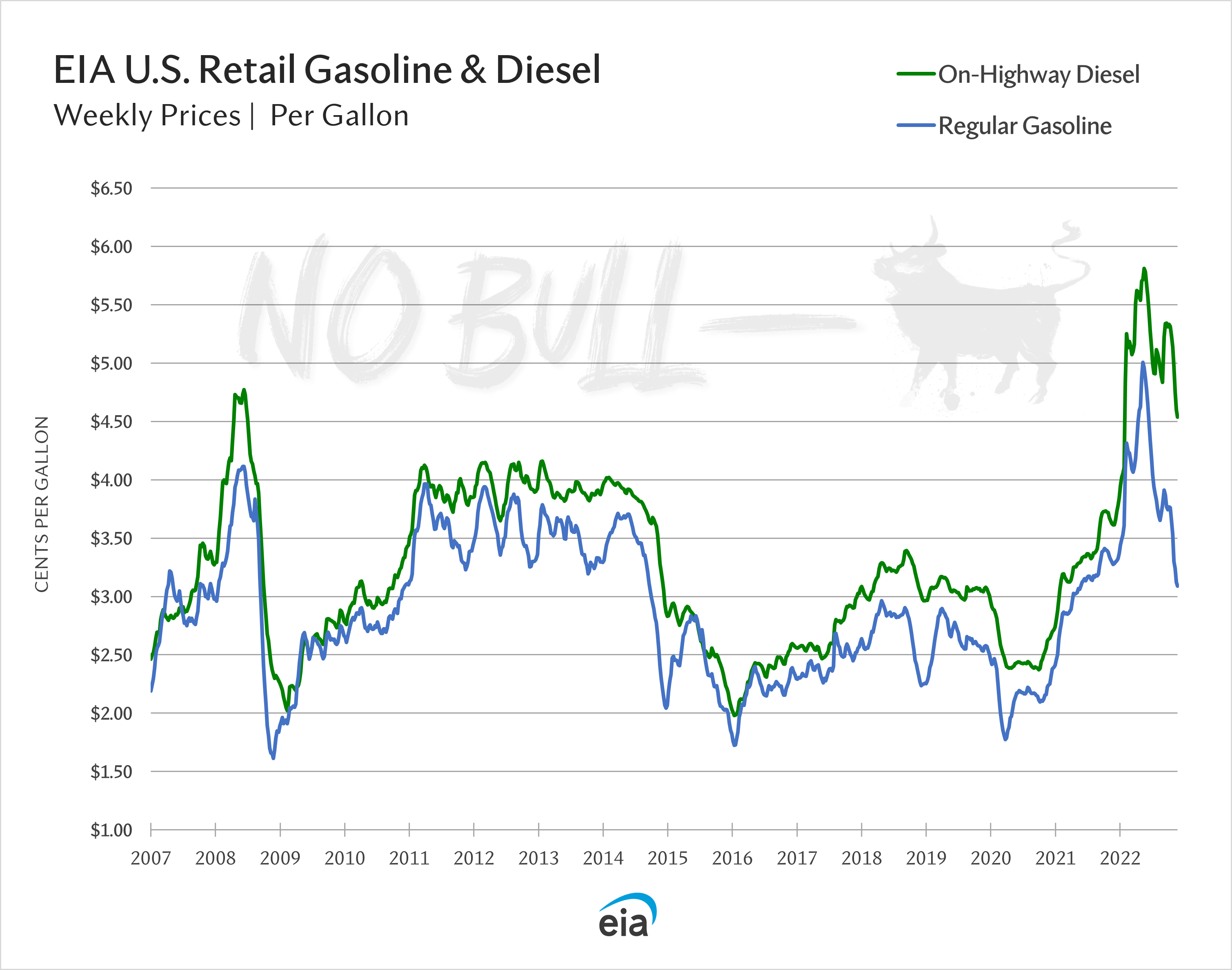

Look at all that green in 2022…

Winner of the Year: Diesel Futures

The biggest winner of 2022 is technically a loser for the farmer - as diesel futures are up nearly 50% YTD. Fortunately retail diesel prices are now more than $1.25 off their summer highs as reported by EIA earlier this week but remain nearly $1 higher than one year ago.

Soybean meal was also a notable winner in 2022, rallying off oilshare unwind and Argentina’s drought to move $60 higher in the past month alone.

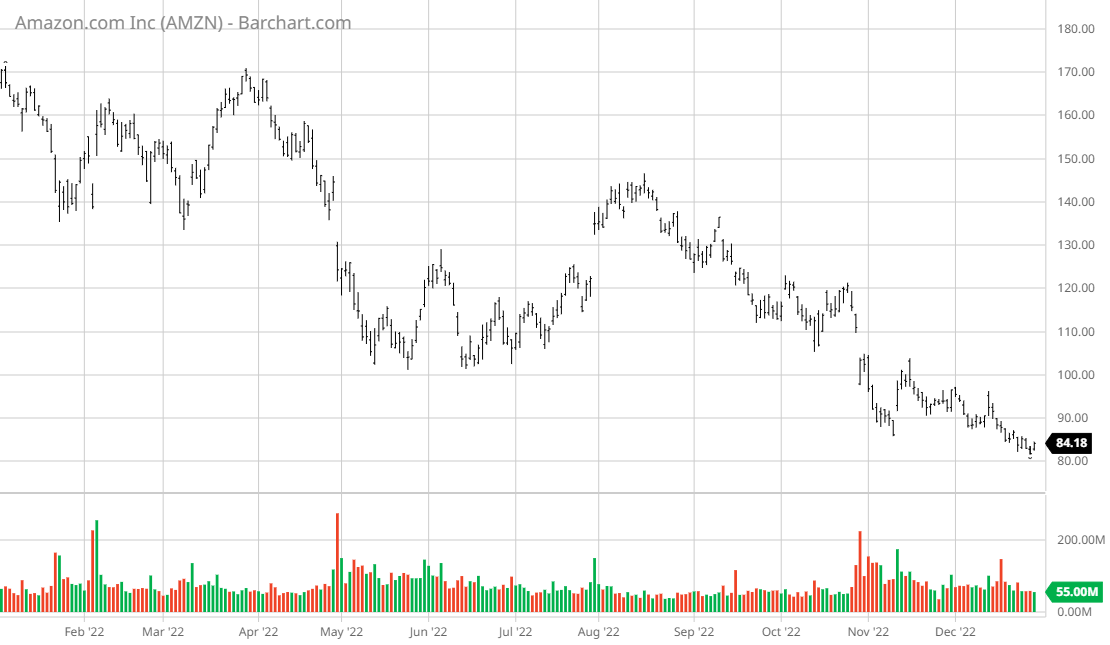

Loser(s) of the Year: Lumber & Equities

Lumber (-61.5%) and equities are the year’s biggest losers as a slowing housing market and recessionary fears loom. Tech stocks saw the largest losses in 2022, with the big ones like Amazon, Meta and Tesla down >50% on the year.

#9 | The Avian Influenza Outbreak of 2022

While I wouldn’t call 2022’s record-breaking bird flu outbreak a major commodity market moving event, it is still quite impactful if you farm in an area that has experienced large bird losses (eg: you lose 1 million chickens on one farm in one whack, there is no longer a need to buy corn to feed them).

Collectively, poultry consumes more US corn than any other species each year; around 1.8 billion bushels or 13% of the 2022 crop.

On top of that, broilers, turkeys, and laying hens account for two-thirds of domestic soybean meal consumption. Broilers alone account for half!

More than 300 commercial flocks have been impacted to date, resulting in the loss of more than 57 million laying hens, broilers, turkeys, and duck or gamebird species.

Layers have been hardest-hit numbers-wise as more than 44 million have been culled to date. Reason being, laying hens are frequently kept in large bird complexes and when one barn on the premises tests positive - the entire farm must be eradicated.

More than layer 20 outbreaks have been in excess of one million birds, two of which have been over five million lost at one time.

As a result egg prices have been on the rise for weeks as continued bird flu losses have sent inventories to historical lows and prices to new highs - above $5 for the first time in history.

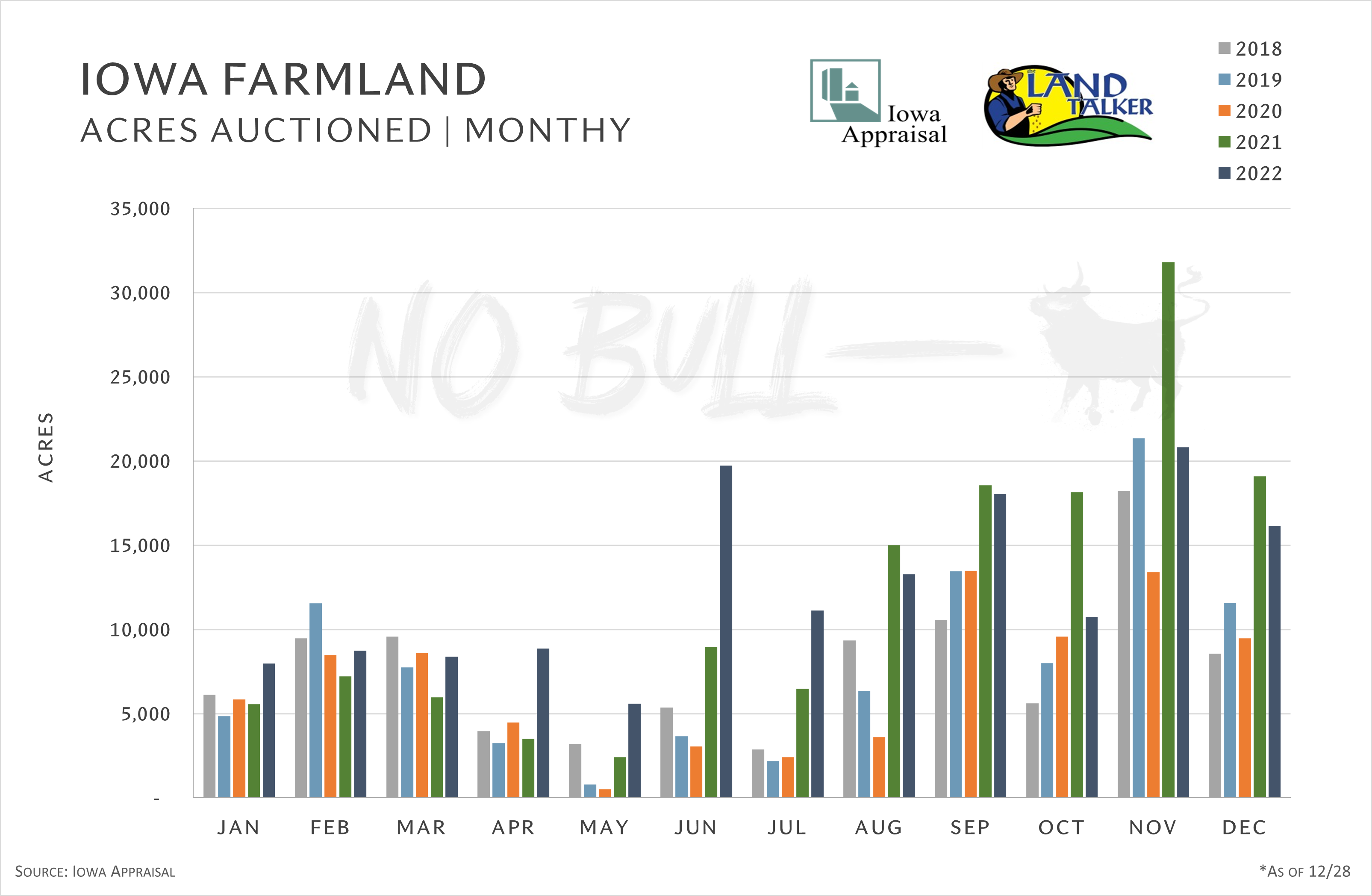

#8 | The Land Rush of 2022

Stat of the Year:

In 2020, not a single farm sold for more than $20,000 per acre in Iowa. In 2021, 16 farms crossed that threshold. This year, as of October, more than 50 (at least one farm every month) has sold for more than $20,000 per acre.

Those lines were pulled from a story by Sara Schafer on AgWeb. Check it out HERE.

In fact, 2022 is the first year Midwestern farm ground broke into the $30,000-an-acre club, as 73 acres in northwestern Iowa sold at $30,000/acre during an auction on November 11.

According to Jim @TheLandTalker Rothermich, more than 16,000 acres of Iowa farmland have been auctioned so far this month which brings 2022’s cumulative total within spitting distance of 150,000 acres.

2022’s sales have officially surpassed 2021’s by a narrow margin - both of which are substantially higher than any years prior.

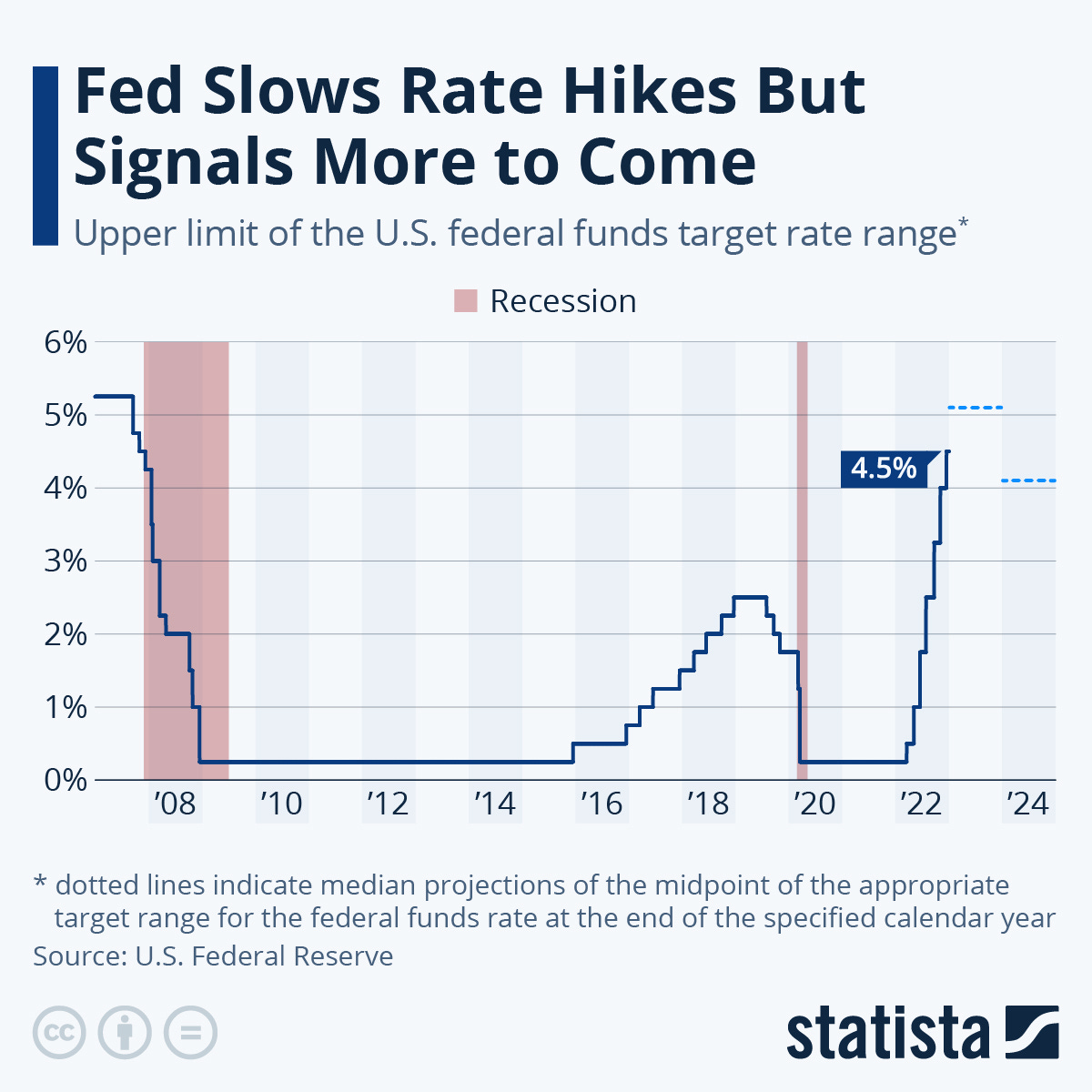

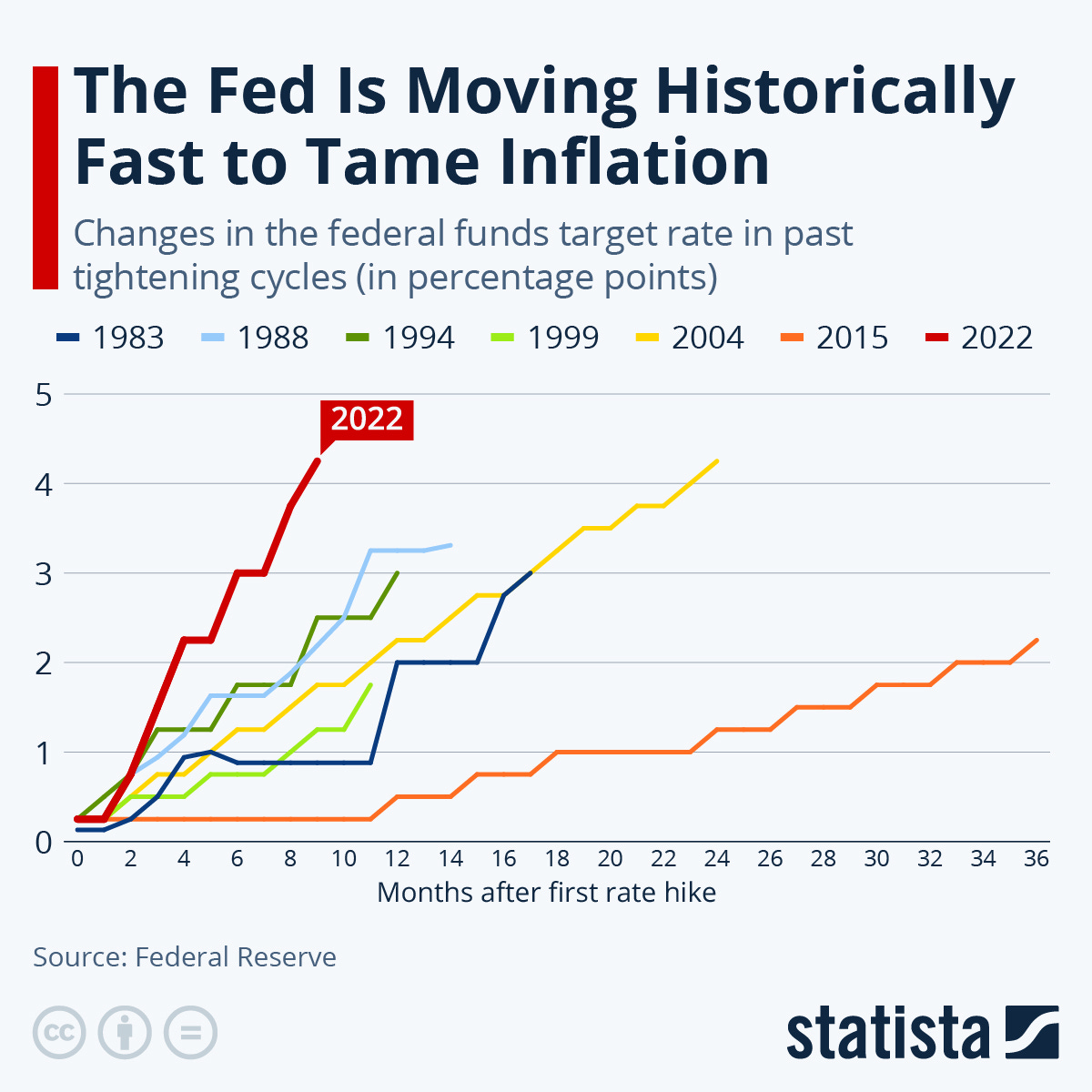

#7 | Rate Hikes

We might see a bit of a slowdown in the land rush in 2023 after the Fed’s historically aggressive action in 2022.

The Fed dished out seven rate hikes in a row this year although December’s 50-basis point hike was a slowdown though compared with four consecutive 75-basis point hikes previously.

The Fed’s action in 2022 is the most aggressive in history.

Although rates were hiked an equal 425 basis points in 2004 through 2006, the tightening was spread over 2 years versus the current tightening cycle of a mere nine months.

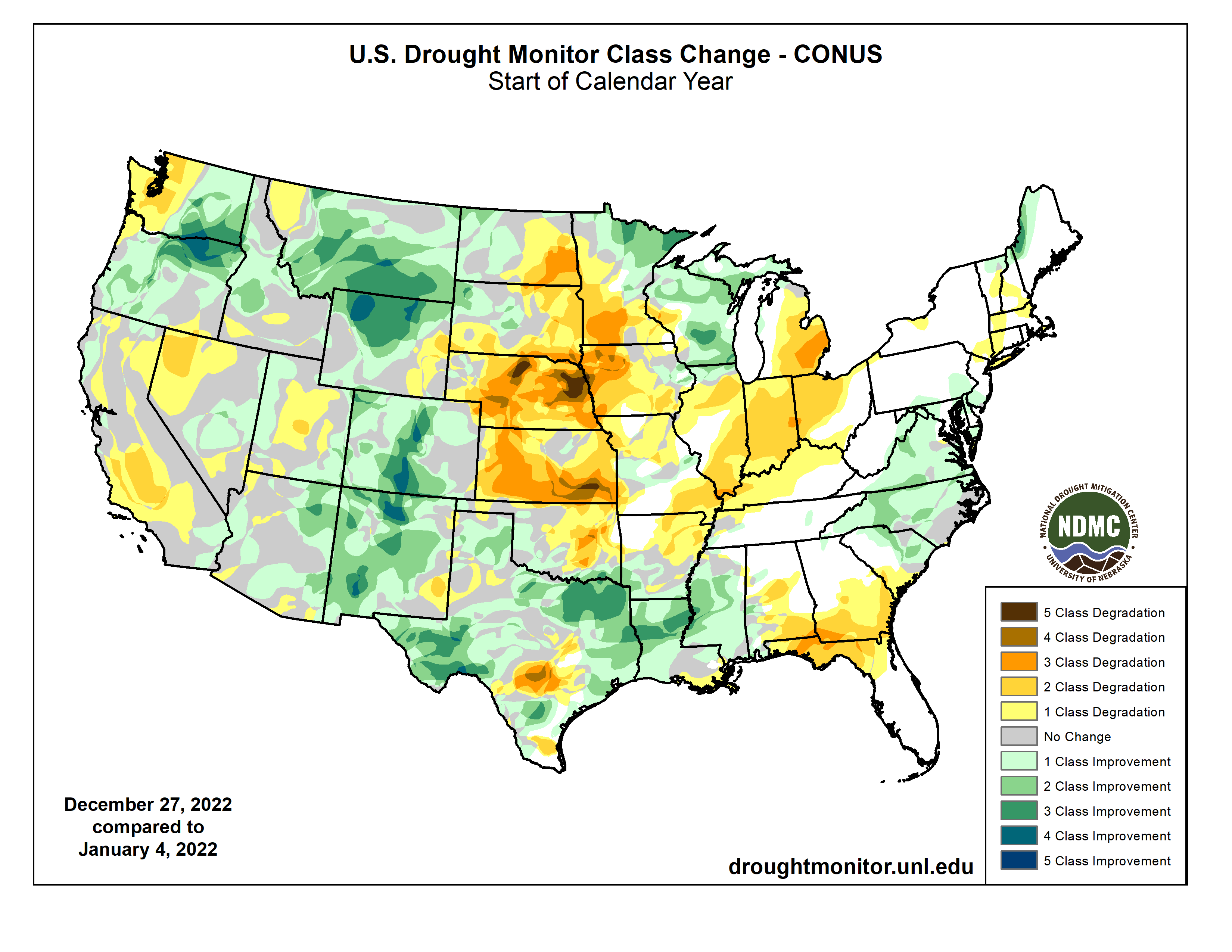

#6 | The Weather

Some areas of the US remain in a world of hurt:

The degradation in conditions during 2022 has been severe:

Many regions saw some of the driest stretches on record from the start of the planting/growing season through end of the year:

As a result - crops suffered in 2022, leaving a large corn deficit to be dealt with in the West and across the Southern Plains.

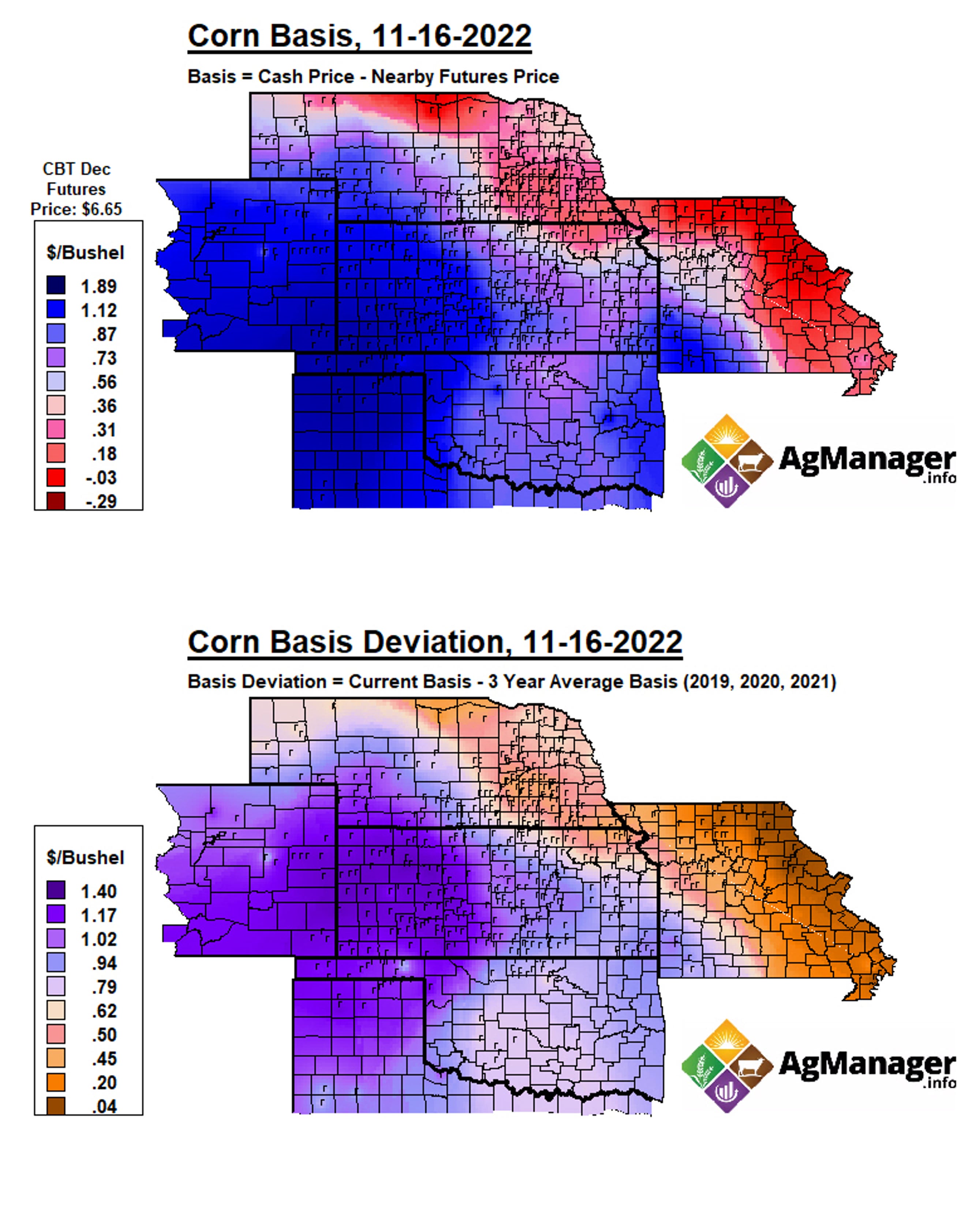

Corn production in SD, NE, KS & TX was a combined 600 million bushels less in 2022 than last year:

The compound effects of short crops in 2021 (KS) plus a drought-stricken 2022 wheat crop and devastating corn losses this year pushed basis levels in some markets to historically high levels:

Feeders in western Kansas and the Texas Panhandle were hit especially hard as short crops left them reeling for bushels:

Where there is a will there is a way though as extreme basis differentials always have a way of solving the problem at hand.

With river logistics a mess and barge freight at record highs, corn has begun working its way west via rail to solve the deficits in the Southern Plains.

#5 | The River

Speaking of the river - the not-so-Mighty Mississippi made mainstream news in 2022 thanks to record low water conditions.

Memphis broke its own record again, one day after I made the image below. The all-time low was set on October 18 at -10.79 feet.

In early October, American Commercial Barge Line reported a total of 185 boats with 2,892 barges were stuck waiting to transit the area around Stack Island, Mississippi - the largest river closure on record.

Low water conditions caused tow size restrictions as well as reduced barge drafts throughout the system - meaning more barges (and boats) were needed to move the same amount of bushels.

As a result barge freight rates soared to record highs this fall and remain nearly 2.5X higher than the 5-year average in St. Louis:

The Mississippi was not alone in the low water nightmare. This image (courtesy of Ballard Drone) is of the Ohio River at Mound City, IL in early October:

#4 | All Aboard for a Rail Strike!

America has been a dominant force in global agriculture thanks to the fact we are home to the most efficient transportation system in the world (Inland Waterways System).

In 2022 we found out just how invaluable that system is… plus we were quickly reminded of the importance of rail as it relates to agriculture as we narrowly avoided a strike not once but twice this past year.

#3 | Exports

Exports turned into a major focal point in 2022 especially as snarled river logistics looked to really limit our ability to ship bushels this fall - during the height of the US soybean export season.

Exporters persevered though, fighting though logjammed barges to even crank out one of our highest soybean exporting weeks on record in October.

Despite all the challenges, soybean export commitments are up 60 million bushels year-on-year as of the week ending Dec 15.

This is largely in part to sizable crop losses in the Southern Hemisphere as the effects of La Niña whacked one billion bushels of bean production off of initial crop estimates.

Corn on the other hand… eeekkk.

Total commitments are down nearly 750 million bushels year-on-year led by China (-335mbu), Canada (remember, they had a drought in ‘21) and some of our most routine and long-standing corn customers like Columbia, Japan, and Mexico:

USDA has reduced their full-year estimate of 2022/23 corn exports four times since July - with the reductions totaling 325 million bushels.

The scary thing is corn sales are STILL lagging the seasonal pace needed to hit USDA’s current full-year estimate by nearly 300 million bushels.

Woof.

We can’t talk about exports without mentioning Argentina as September’s Soy Dollar program gave producers an immediate bump in prices received at the farm level, encouraging record amounts of farmer sales during that time.

As a result Argentina exported a record amount of beans in October - which is a big change for the soybean processing capital of the world.

While Argentina generally accounts for 12% of world soybean production, they only have 4% of the global export share as 80% of their soybeans are crushed each year.

Argentina decided to try a second round of the Soy Dollar program this month, but producer sales to date have been underwhelming to say the least.

#2 | Russia’s Invasion of Ukraine

It has been 309 long days since Russia invaded Ukraine on February 24, 2022.

In the days following initial attacks, nearby Chicago wheat futures rallied more than $5, north of $13.60 while KC futures hit a high of $12.99-1/2.

Today, March SRW futures sit more than $1 below where they were when the invasion happened while March HRW futures are 25 cents off pre-war levels.

In the time since late-February, we have all had a fast lesson in the importance of agriculture in the Black Sea region. Russia and Ukraine play a significant role in the production and exports of sunflower seed (oil, in particular) and many feedgrains.

Agriculture is the most important sector of Ukraine's economy representing 45% of total exports as the industry accounts for 9.3% of GDP.

Turns out that trade war headlines and real war headlines have the same effect on the market - ups and downs, twists and turns and by the time the dust settles no one knows what is really going on.

Lord knows we saw our fair share of headlines in 2022, especially as the infamous Grain Export Corridor was established late-summer followed by an extension last month.

#1 | All Things Green

2022 has been green, green, and more green.

From green diesel to green initiatives - there has been a major ‘green’ theme this past year.

Renewable diesel continues to take the US by storm, with nearly 700 million bushels of added annual crush capacity announced the past few years.

I have some work to do on this map as there have been a few new plants announced in recent months plus I have some tweaking to do on previously announced projects.

Either way - you get the point. The face of US soybean demand is changing right before our eyes.

The green diesel boom has led to a run on soybean oil - once considered the ugly, red-headed stepchild of the crush complex, is now a hot commodity itself.

As a result, crushing soybeans has been like printing money (hence all the aforementioned new plants and expansions).

Another type of ‘green’…

Headline(s) of the year:

Like it or not - the green initiatives are not going away.

EPA’s long-awaited Renewable Fuel Standard blending obligations for 2023-25 was finally released the end of November, proving to be a major disappointment as they pivot away from traditional crop-based biofuels and towards biomass-based renewable energy sources that will generate electricity for EVs.

Shocker of the year: The eRIN

In a first, EPA proposed an eRIN credit awarded when electricity from certain renewable sources is used to power EVs. The eRIN introduces a pathway for electric vehicle makers like Tesla to generate credits, just as an ethanol plant or biodiesel facility would.

This credit is designed to further encourage the production of EVs, helping with the U.S. goal of net zero by 2050 and piggybacking off of the Biden Administration’s Inflation Reduction Act (aka the big, green bill) that was passed earlier this year.

And with the stroke of a pen the government giveth and the government taketh away.

That is all I have for you in 2022.

Have a happy New Year, I will see you in 2023!