AgriNext details can be found HERE, including agenda and full speaker list.

Only one week remaining to save $100 with Early Bird registration. Visit NoBullAgriNext.com to register!

Weekend(er) Teaser

Can you correctly identify each line in this week's Weekend(er) Teaser?

Hint: two commodity markets that are completely unrelated

Keep reading for the answer!

In this weekend’s update:

The continued KC vs. Chicago wheat cage match

WCB forecasts = feeding the bulls

The 2.3bbu corn puke that has left funds at a crowded intersection

Rumors & social media posts are running the soy complex

Weekend(er) Teaser reveal

Meal matters + the RVO update you need to know

Headline(s) of the week: Big Beautiful Bill, update on Brazil HPAI, & the craziest Texas traffic stop involving haybales

Brazil Safrinha corn update/mini tour of Iguazú Falls

No Bull’s next AgVenture —> Brazil in February 2026

Weekly Winners & Losers

Both Kansas City and Chicago wheat saw a bump last week, up 22 and 17 cents, respectively on the week, despite lower closes on Thursday and Friday.

Both KC and Chicago have rallied off their mid-May lows but SRW remains the stronger of the two as an unexpectedly high March 31 production number and prospects for another year of burdensome stocks has left HRW under pressure.

HRW's premium over SRW peaked at 40 cents but has steadily declined, reaching a 9 cent discount before firming slightly to end the week.

Funds’ net short position in KC wheat at -80,162 contracts sits just shy of the all-time record short of -80,799 set the week prior.

Meanwhile, Chicago wheat also holds a large short at -116,647 contracts, though it remains about 20% lower than its all-time record short.

Managed money’s net position in KC vs Chicago is closely correlated with KC’s premium over Chicago futures:

Starting to hear chatter with concerns for SRW quality as some areas continue to struggle with too much precip.

Oklahoma into northern Arkansas, southern Missouri and continuing to the northeast along the Ohio River have seen one of their wettest April/Mays on record:

Wet conditions have also slowed planting progress in some areas where are much as 200% of normal precipitation has fallen in recent weeks.

On the other hand, there is mounting dryness in the western Corn Belt, where a fraction of normal precipitation has fallen since April.

The problems are becoming more obvious by the day in the west where drought conditions continue to intensify, especially in Nebraska:

Quite the change year-on-year:

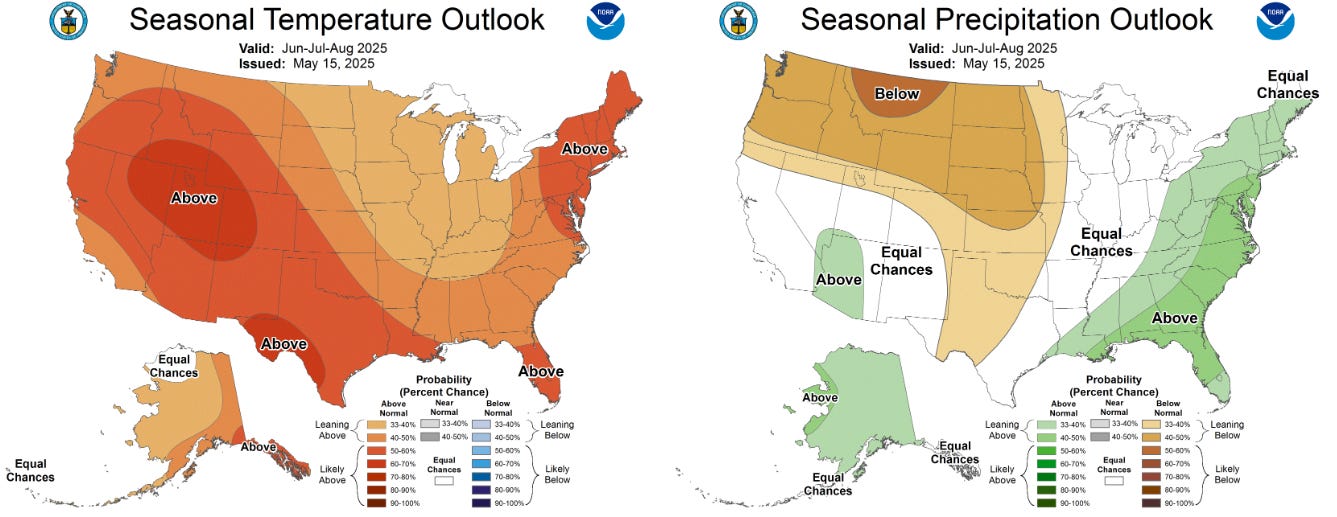

Weather watching season is officially underway and the long term forecast is giving the bull something to chew on:

Current drought conditions in the west are likely to persist, while drought expansion is likely into the N Plains and areas to the east in the western Corn Belt:

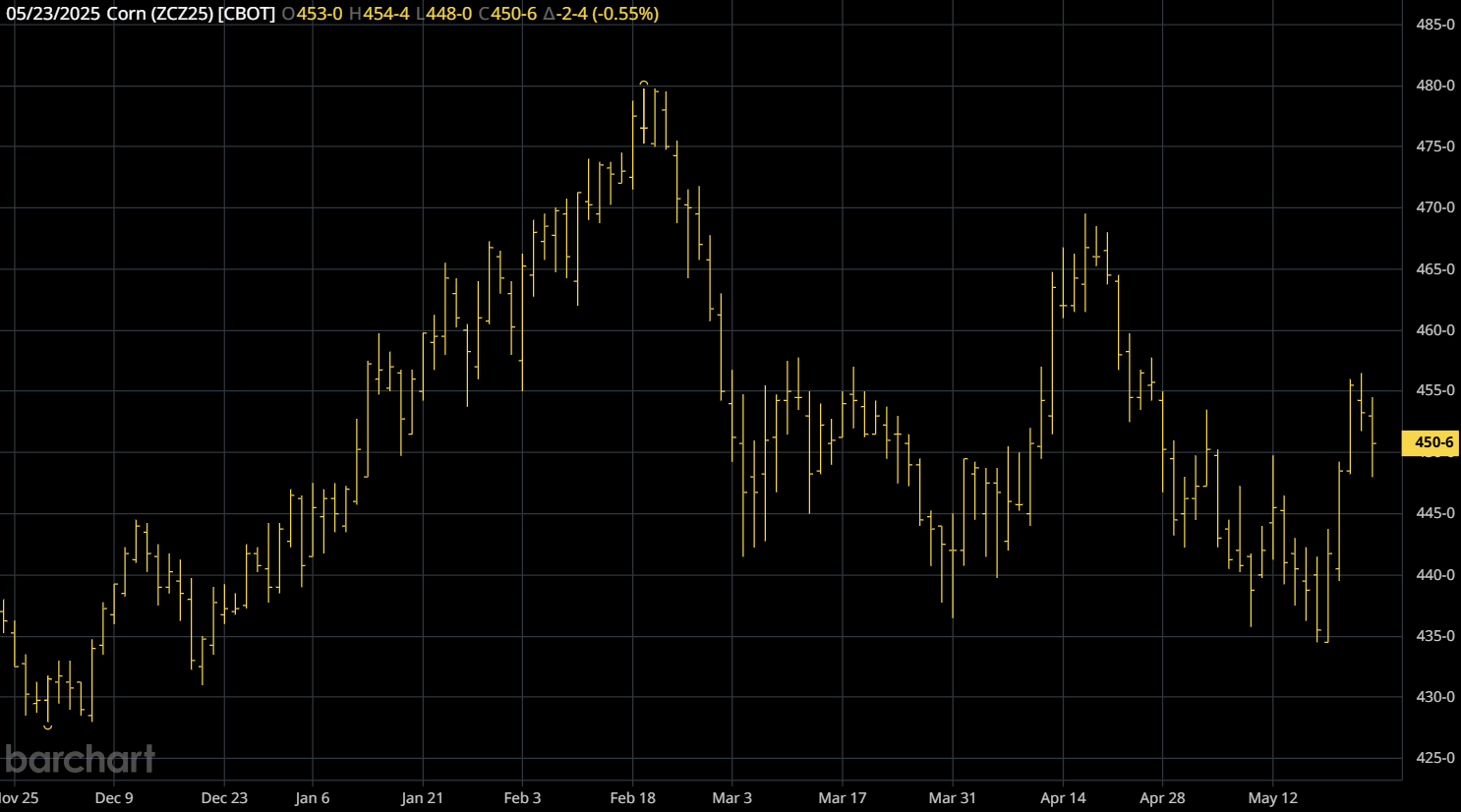

Dec corn gave back a bit of its gains end of the week but still managed to close near $4.51 on Friday, up 15 cents on the week:

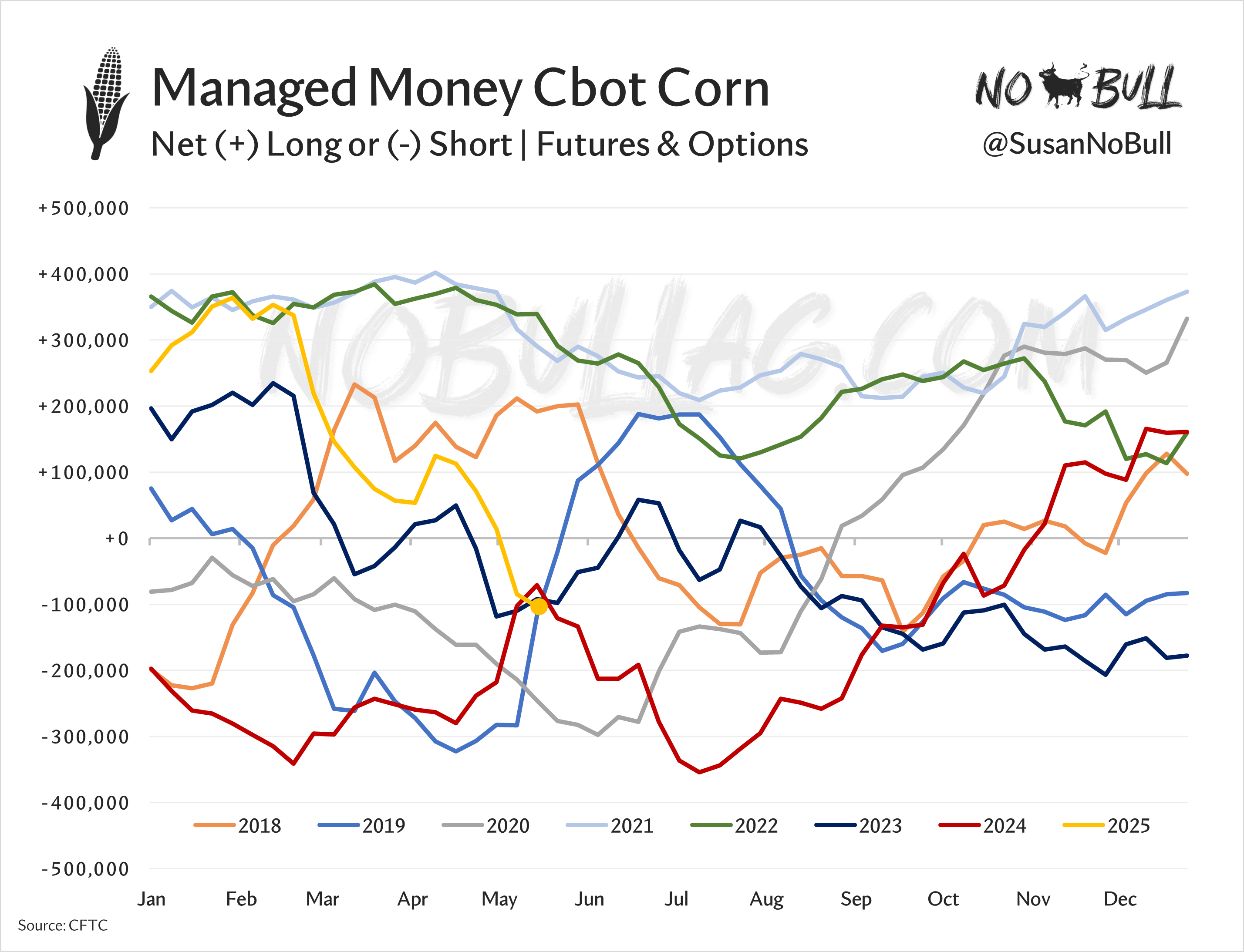

Managed money dumped length in corn for the 5th week in a row last week, driving their net short to -103,210 - the first time funds have held a net short in the 6-figures since September.

Since we saw the net long peak in early Feb, funds have dumped ~2.3 billion bushels and front-month futures have collapsed 50 cents in that time.

Interesting to note that today’s net short is very similar to the position at this point in 2019, 2023, and 2024:

Here’s a side-by-side look at the past three years comparing net position with price:

Keep reading with a 7-day free trial

Subscribe to No Bull to keep reading this post and get 7 days of free access to the full post archives.