HOT Nugget

In the coming weeks I will release a series of subscriber-only updates, recapping last week’s Summit 24 - Wheels Up | Taking Agriculture to New Heights.

Today, though, I want to start with what is undoubtedly the HOTTEST topic in agriculture where time is truly of the essence as U.S. corn ethanol demand and ultimately U.S. corn demand are both on the line.

Check out the way U.S. corn demand has evolved over time:

Thirty years ago, feeding and exports accounted for 90% of corn demand.

Today, feed continues to hold the largest percentage share of demand but it runs neck and neck with domestic ethanol demand, who has been the predominant driver in demand growth since the Renewable Fuel Standard’s inception nearly 20 years ago.

Same thing, different view:

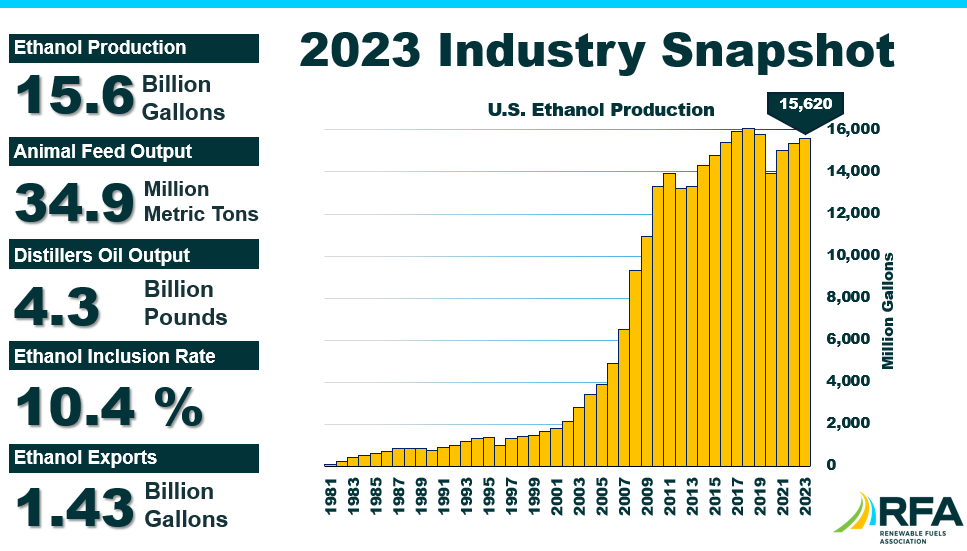

As a result of the U.S.’ desire to reduce emissions and protect our energy independence, ethanol production has grown to more than 15 billion gallons annually - accounting for one of every two gallons of ethanol produced in the world.

The problem is… U.S. production growth has stagnated:

And what happens if that 5 billion bushel+ of annual corn demand starts to take a step backwards?

It isn’t just about the big picture impact to the US balance sheet… it’s even MORE impactful at the farm level.

This about it - if your local ethanol plant reduces their grind or calls it quits altogether…

Basis tanks and YOUR balance sheet begins to take a hit.

Love them or hate them, biofuels are a big part of agriculture and an even bigger part of the rural economy…

and….

Love it or hate it, Summit’s CO2 pipeline plays an instrumental role in where biofuels (and corn) go from here.

WHY?

Sustainable aviation fuel presents a tremendous opportunity for US agriculture - corn ethanol in particular.

Renewable jet fuel production is literally taking off in the United States as the airline industry aims to meet emissions reductions targets set forth by the Federal government.

The Biden administration’s Grand Challenge has a production target of 3 billion gallons of SAF annually by 2030.

IF* those 3 billion gallons of SAF were produced entirely out of corn ethanol - it would add more than 5 billion gallons of ethanol demand each year - an increase of 33% from current levels.

Plus, demand will only grow from there as it is estimated we will produce 35 billion gallons of SAF annually by 2050.

(*won’t happen with 100% corn ethanol, just illustrating the point)

Unfortunately, there’s a catch.

SAF is 2-2.5x the cost of kerosene jet fuel, making it cost-prohibitive to both produce and use…

(enter ‘the government’, stage left)

In the newly-emerging SAF market’s infancy, the government is helping buoy the cost of production with tax incentives laid out in the IRA.

The kicker is, the carbon intensity score of SAF made from US corn ethanol is TOO HIGH to qualify for the tax credit (yellow bars/orange line).

The ONLY WAY US CORN ETHANOL CAN MAKE ITS WAY INTO SAF PRODUCTION IS VIA CARBON CAPTURE & STORAGE (CCS - green bars).

CCS 101: Carbon dioxide is released into the air as a result of the fermentation process during ethanol production, accounting for a sizable chunk of corn ethanol’s carbon intensity score.

During carbon capture and storage, that CO2 is captured, compressed, and stored underground in deep geologic storage sites.

Seems easy enough, right?

It takes a particular type of underground geological formation to effectively hold on to CO2.

The good news is the US has several such areas (tan):

The bad news is they are largely outside of the corn belt, leaving much of the US ethanol capacity out of luck:

Corn-producing parts of the country with geology suitable for carbon capture & storage are limited to a large part of North Dakota and Illinois.

As a result dozens of existing plants are left helpless with a CI score too high for their ethanol to be used as a feedstock in SAF production.

Now, THIS is where we get back to last week’s conference event and the morning session, From Field to Flight, with Summit Agricultural Group CEO, Justin Kirchhoff.

I came into last week’s event hoping to deepen my understanding of SAF and the opportunities ahead for US agriculture.

I left with my eyes opened, as SAF isn’t a matter of IF but WHEN…

…and when this jet takes off - we better make sure agriculture is on board!

As a solution to the problem (dozens of ethanol plants across the Corn Belt do not have direct access to carbon capture sites), Summit Carbon Solutions aims to build 2,500 miles of pipeline to transport CO2 from 57 ethanol plants to a sequestration site in North Dakota.

Those 57 plants produce 6 billion gallons of ethanol each year, accounting for almost 40% of US production.

Better yet, Summit’s pipeline provides value-add for those 57 ethanol plants as they not only realize additional revenue from sequestering their carbon, but their corn ethanol now qualifies as a feedstock in SAF production.

This increases plant margins, production capacity and ultimately, their bid.

Plants with access to a carbon capture and storage pipeline or those who are able to sequester on-site will be at a massive advantage to those who are not.

There WILL BE WINNERS AND WILL BE LOSERS and those plants without access to CCS have an uphill battle ahead.

As important as Summit’s work is to the heart of the Corn Belt, they faced early headwinds but it feels like the ag community is beginning to recognize the significance of the project.

I hope that today’s recap sheds light on the importance of a pipeline to the long-term viability of the US ethanol industry and ultimately US corn demand.

Time is truly of the essence as the door opens to the next generation of biofuel demand.

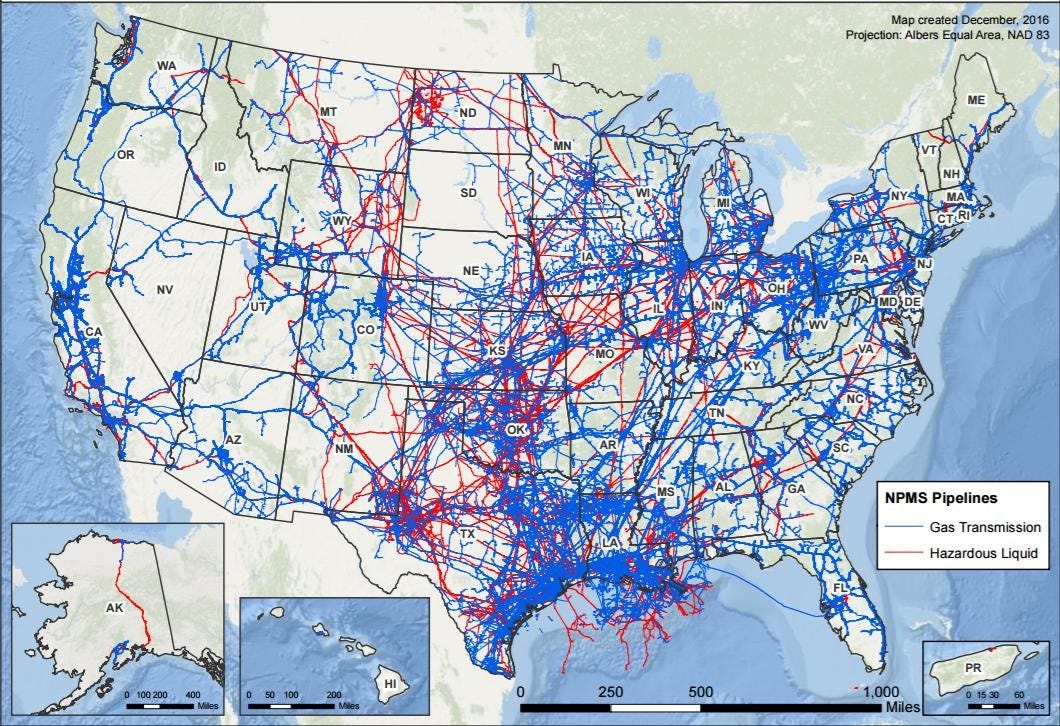

To put Summit’s project in perspective, here is a map illustrating the more than 2.6 million miles (enough to circle the earth 100 times) of existing pipelines in the US, transporting energy products and carbon dioxide to consumers and industries each day, quietly beneath our feet.

It is easy to forget the thousands of miles of pipeline already under US corn and soybean fields today.

Lastly…

Speaking of winners and losers, here is a fantastic visual released by EIA yesterday:

Coal was legislated out of existence for its carbon emissions (case in point above).

We have been fighting for higher ethanol blends for years, only realizing a negligible percentage-uptick during that time.

Today, we are presented with one of the biggest opportunities ag has ever seen, yet we are reluctant to change.

Something’s gotta give, otherwise we are going to miss this flight altogether.

I will be back this weekend.

Thanks!

10/10 👍🏻