10 HOT Nuggets

#10 | June WASDE Corn

The June report is generally a snoozefest and this one was no different as we saw minimal changes across the board.

Corn

There were absolutely no changes to US corn S&Ds - old crop or new. Both Brazil and Argentina production were left unchanged as well which means we will drag the large discrepancies between USDA & private estimates out for another month at least.

Current-year US corn exports could see a revision higher in coming months as sales have been particularly strong as of late.

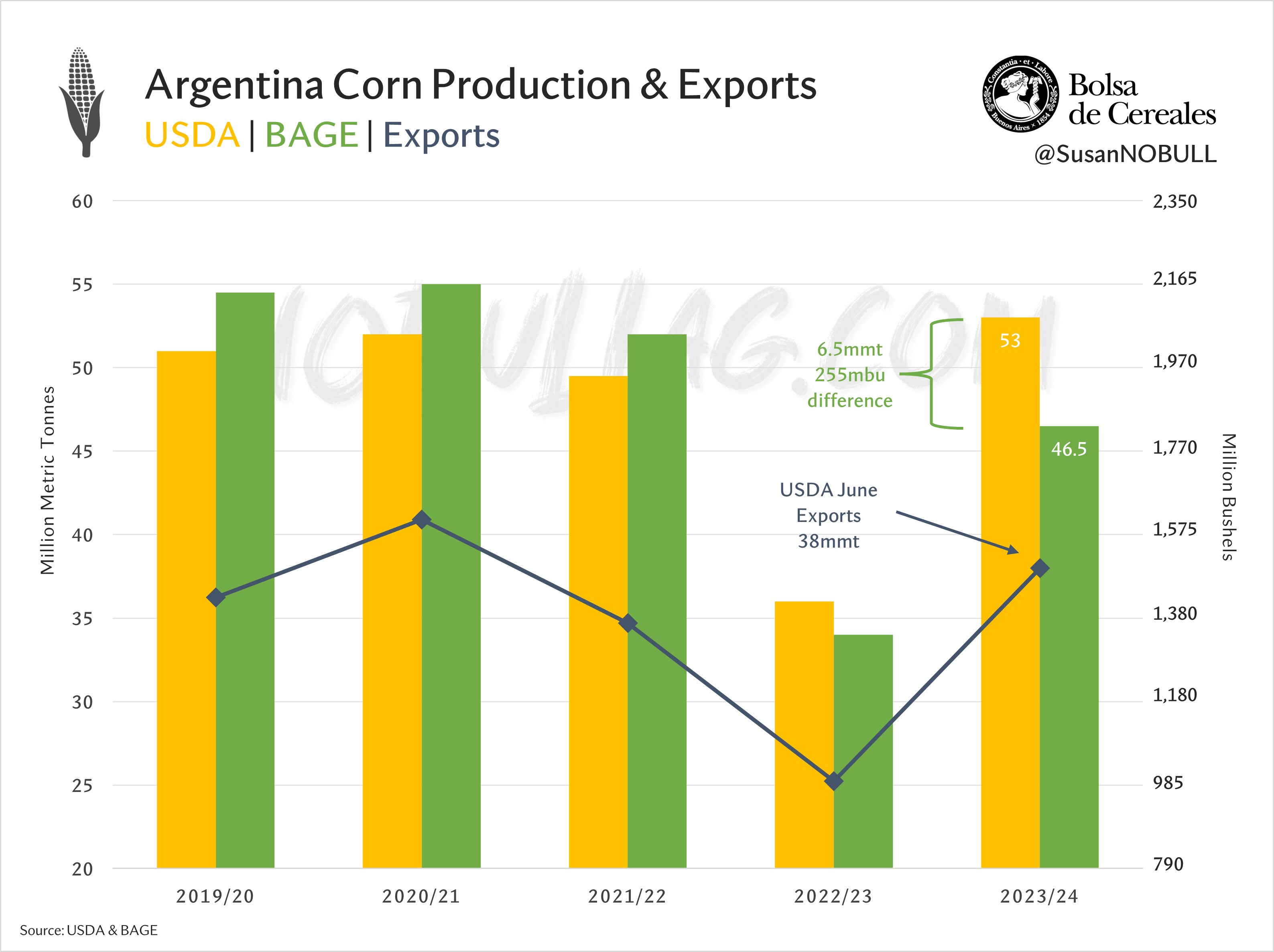

Reminder: USDA Argy corn 53mmt vs Argentine private estimates near ~47mmt (250mbu difference)

USDA Brazil corn 122mmt vs Conab/privates ~112mmt (400mbu difference)

That’s ~650mbu difference that can make a big impact on US corn exports in 2024/25, especially when considering potential production shortfalls in other parts of the world.

#9 | June WASDE Soybeans

We only saw one change for US S&Ds as current year crush was reduced 10mbu (not a surprise), increasing 23/24 ending stocks by the same to 350mbu. That same 10mbu carried over as an uptick in new crop beginning stocks, increasing 24/25 carryout by the same.

In somewhat of a surprise USDA did NOT reduce old crop bean exports, even though we continue to trail the pace needed to hit their current 1,700mbu estimate by >50mbu. While we have seen a string of export sales flashes to China the past few days (more on this in a minute), USDA will still have to make a reduction in July or August.

Brazil’s 23/24 bean crop was reduced 1mmt to 153mmt while Argy was left unchanged.

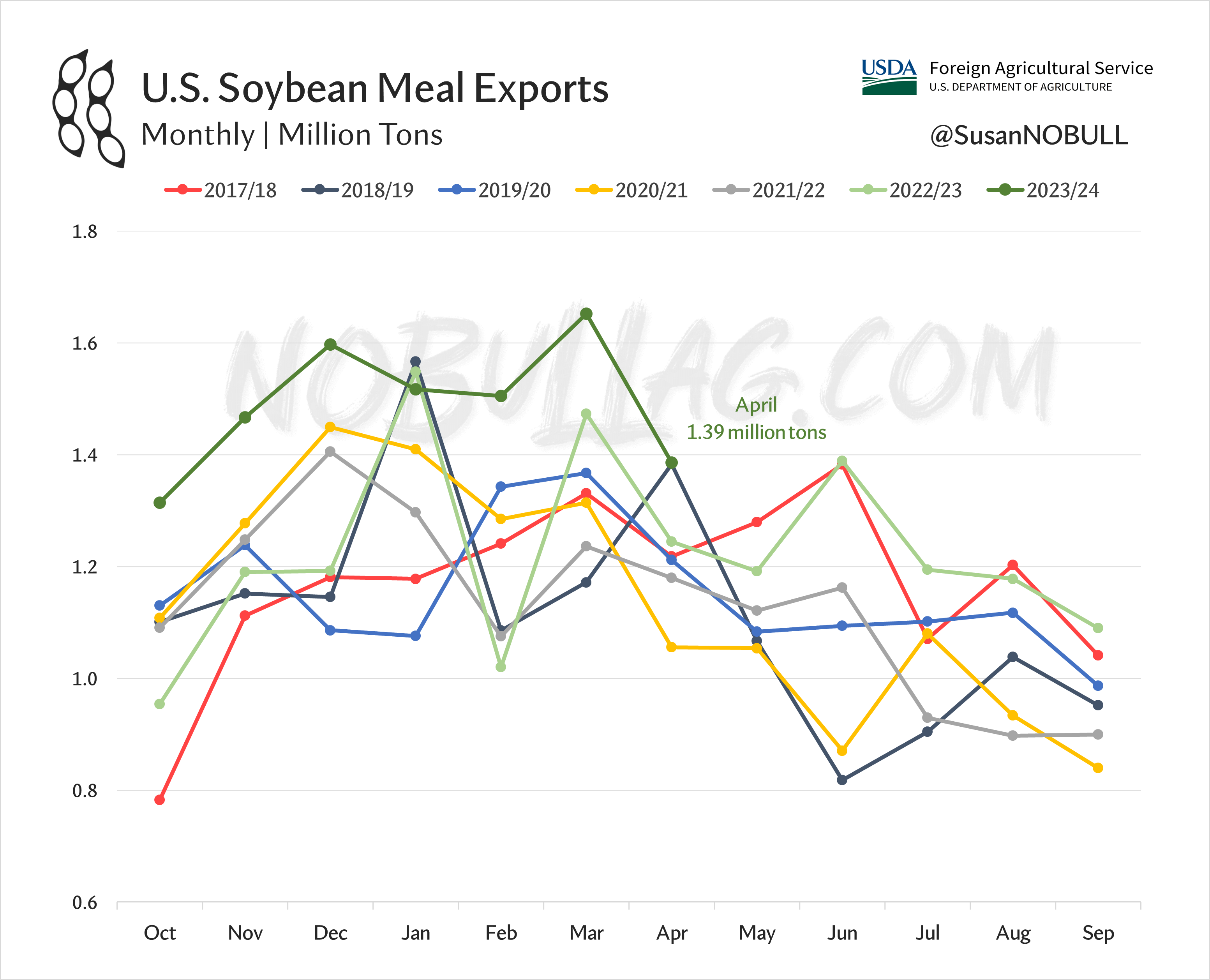

One more thing on soy - US soy products saw increases to exports for both old crop and new as meal sales continue to make records and US soybean oil becomes more competitive in the world market amid sinking domestic basis levels.

April meal exports set a new monthly record, just barely edging out April 2019 at 1.39 million short tons (~58,000 semi truck loads of meal).

Cumulative exports for the 2023/24 marketing year are a record 10.4 million tons - up 21% year-on-year and 17% higher than the prior shipment record set in the 2020/21 marketing year.

And guess what? Records will continue to fall as additional US crush capacity comes online in the next few marketing years.

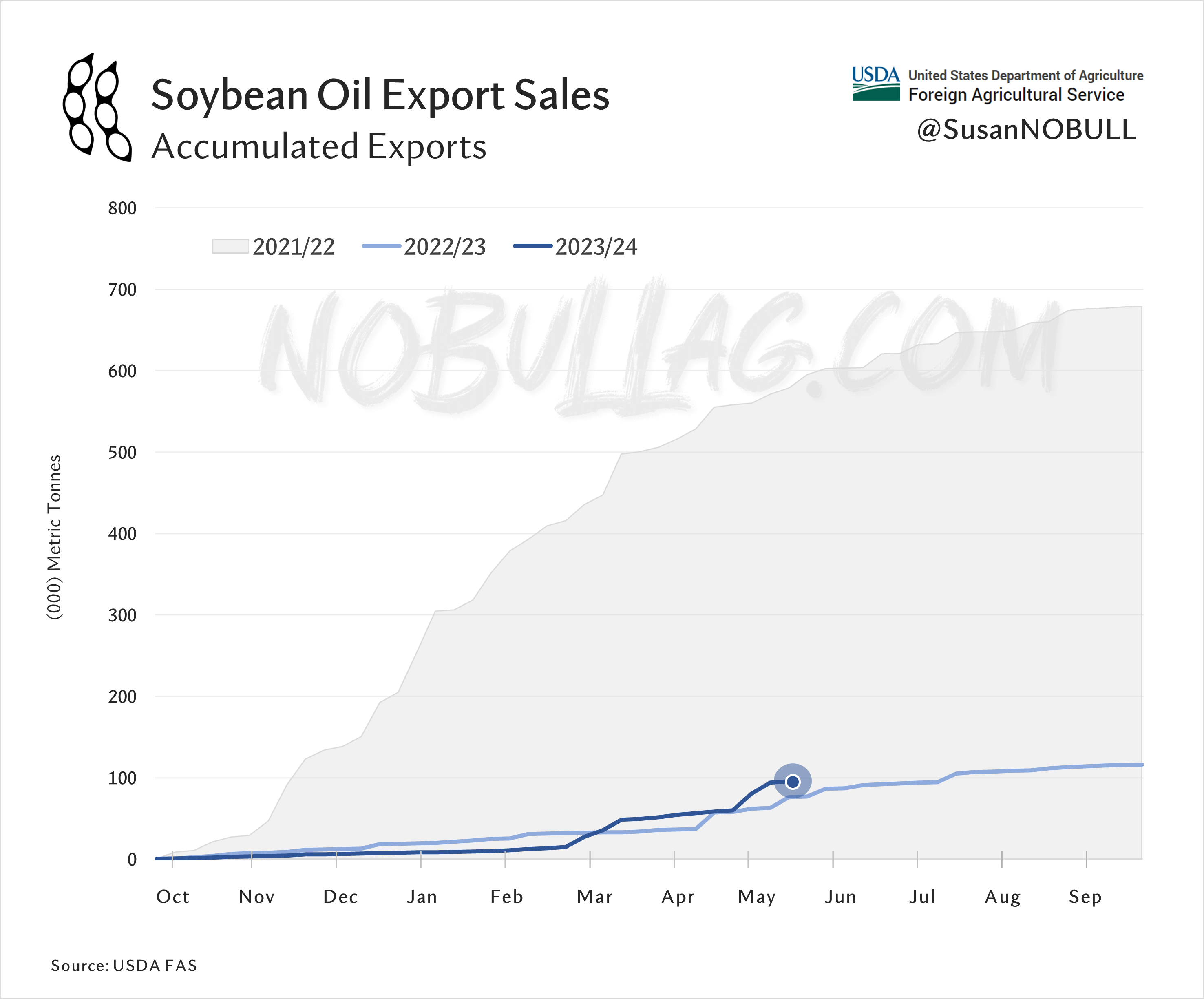

Switching products - soybean oil sales in recent weeks have been monumental compared with the past several months:

Buttt… zoom out a bit and you’ll see we are nowhere near exports of the pre-renewable diesel boom era:

Keep reading with a 7-day free trial

Subscribe to No Bull to keep reading this post and get 7 days of free access to the full post archives.