The Wednesday HOT TAKE

December 17 | Demand shifts that can't be ignored

In this week’s HOT TAKE, we’re focusing on the demand shifts that continue to reshape corn and soybean markets:

« Why crush may be hot while soybean oil is not

« Why U.S. ethanol production continues to shatter records

« Why Brazil’s corn ethanol market is really heating up

« And in today’s HOT Nugget, a new way to look at the crowding out of U.S. soybean exports

What’s HOT & What’s NOT

HOT: NOPA Crush

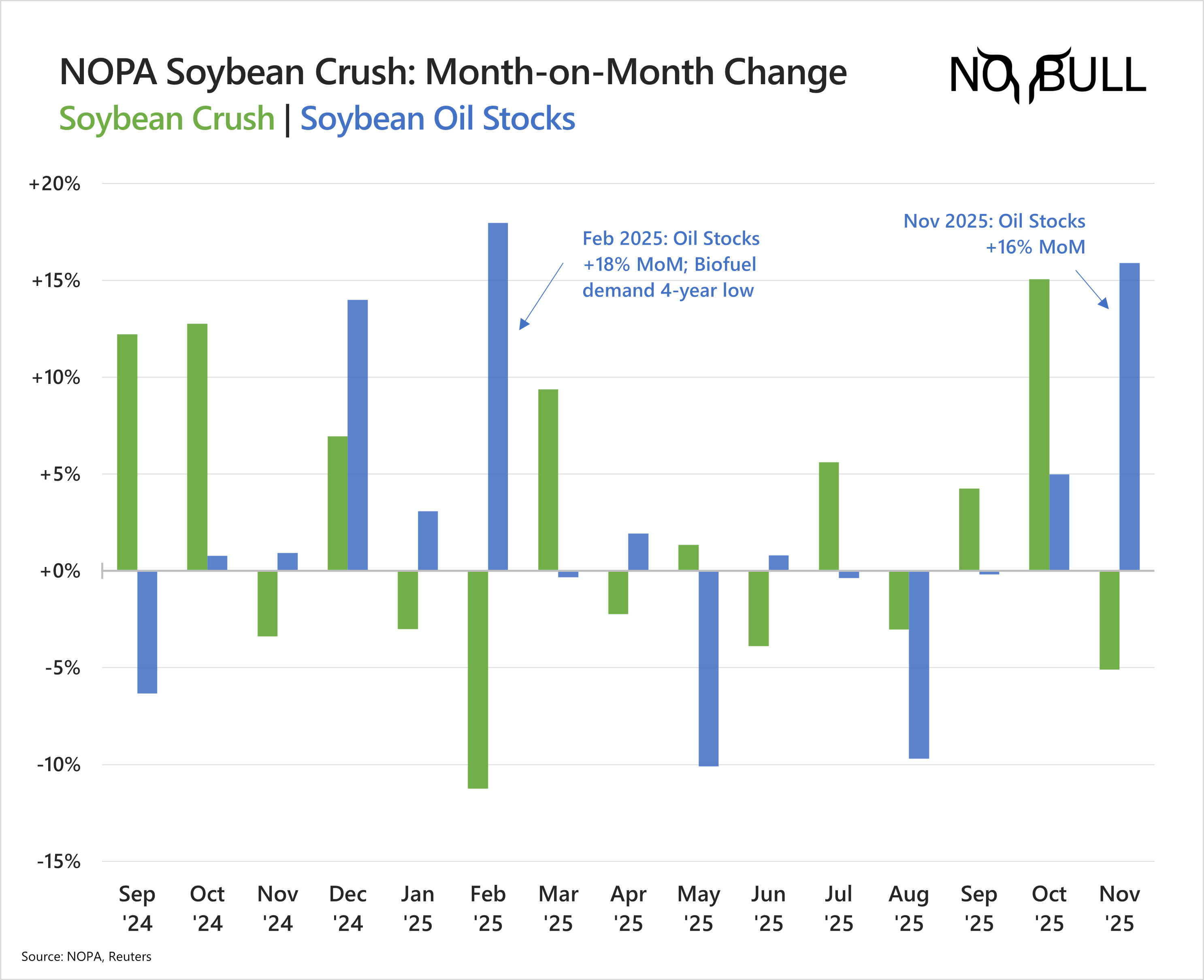

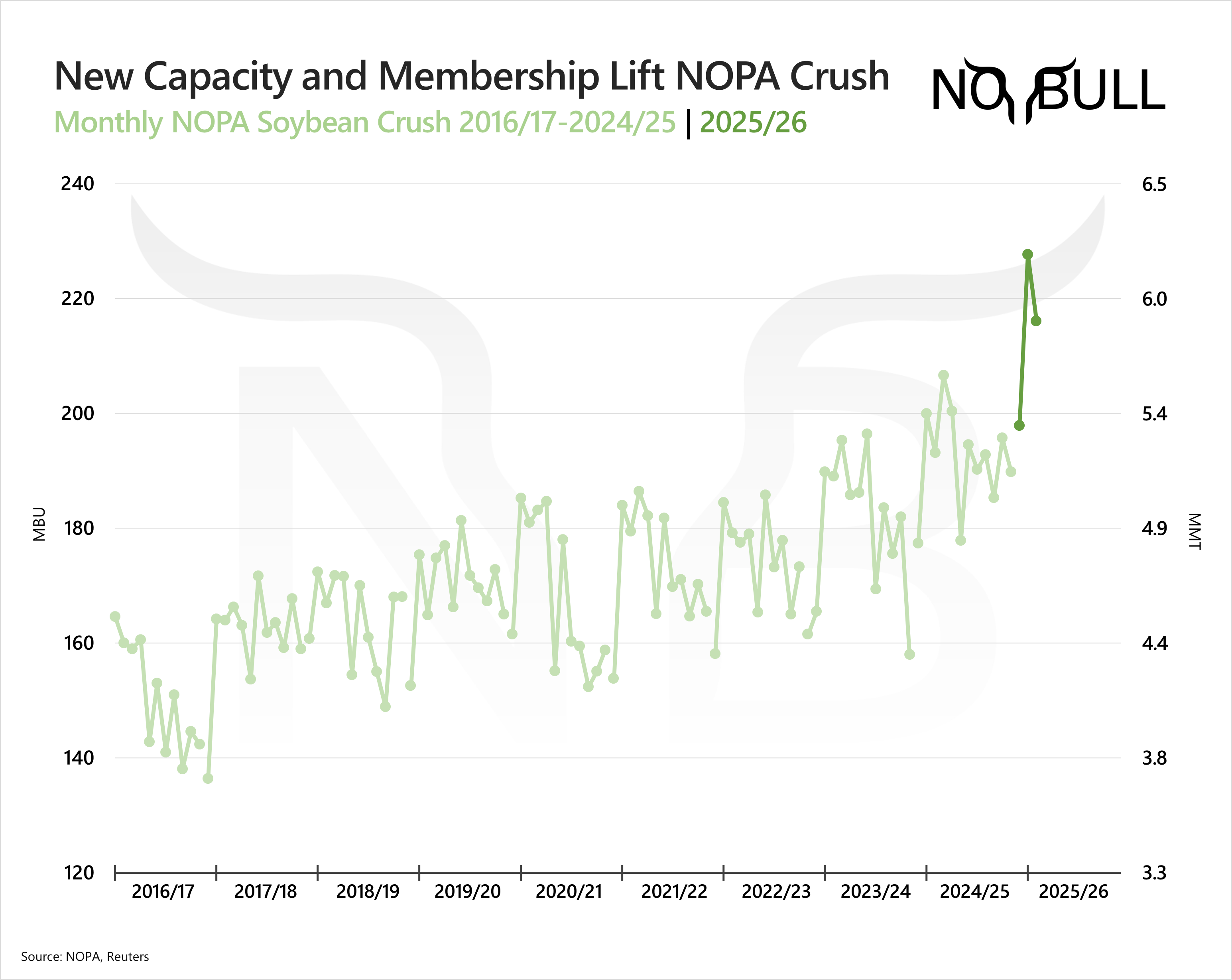

Added crush capacity and expanded membership unsurprisingly pushed November NOPA crush to another monthly record. At 216 mbu (5.9 mmt), November crush blew past the prior November record, though it fell 5% from October — the largest Oct-to-Nov percentage decline since 2019.

NOT: Soybean Oil

The bigger issue was the build in soybean oil stocks, which rose 16% month-on-month to 1.513 billion pounds, despite a 5% decline in bushels crushed.

While oil stocks typically build into winter as demand slows, this increase stands out as the largest monthly build since February 2025 — the same month soybean oil biofuel demand hit a four-year low following the initial 45Z fallout.

The setup feels familiar. We’re heading into year-end with major biofuel policy changes looming and 2026 rules still undefined, leaving renewable producers hesitant to make forward purchases.

The key difference versus last year is that producers were using as much soybean oil as possible, knowing the $1/gal blending tax credit — regardless of feedstock or carbon intensity — would expire at the end of 2024. Today, it’s the opposite. Cash oil is weak, buying is largely hand-to-mouth, and palm oil trading at a discount to U.S. soybean oil is capping export demand.

While attention is on the new monthly record, it’s worth remembering that crush depends on margins — and right now both crush and biofuel margins hinge on EPA finalizing 2026 rules, which will not be known until Q1, confirmed in a notice filed by EPA earlier this week.