What’s HOT & What’s NOT

Love is in the air

No better way to kick off this week’s HOT TAKE than with a few ag-themed v-day cards:

Mmmmhhmmm. There are a few of you who missed this memo:

And last but certainly not least - this little guy wins the price for the coolest valentines cards ever - complete with a glow stick!

Give it a couple years Gavin; I know a little blonde that will be chasing your shiny John Deere Green paint (since that is her favorite song)!

Fueling the fire

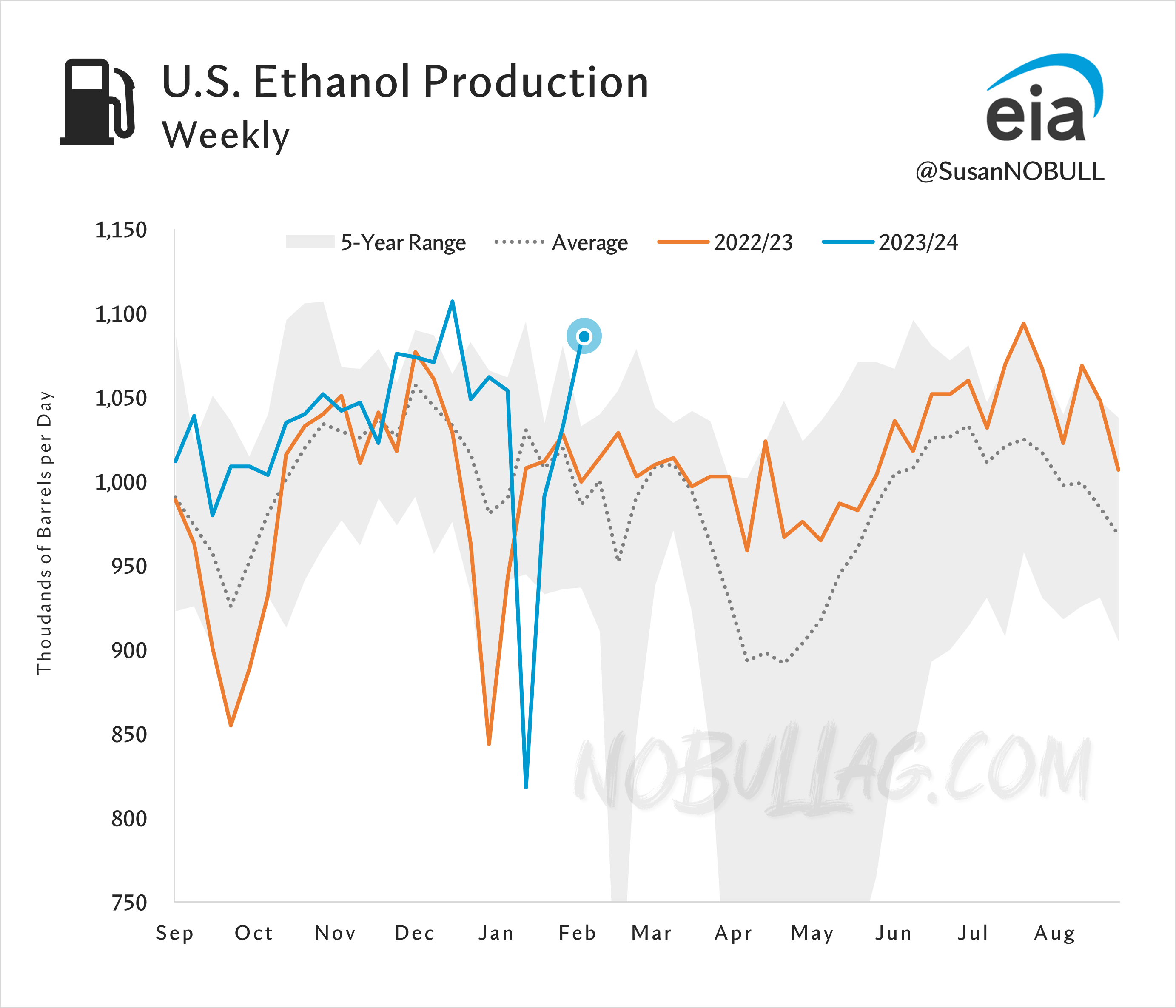

The U.S. saw another big week of ethanol production in the week ending February 9 - 1,083kbpd was a 7-week high (we are in post-arctic blast recovery mode still), surpassing even the highest of analysts’ estimates and eclipsing the prior 5-year high.

Same goes for stocks, at 25.8 million - which fell above the highest pre-release estimate and outside of the 5-year range.

Unfortunately, gas demand (aka product supplied) hasn’t been setting the world on fire either, falling more than 7% week-on-week and sitting 5% below the five-year average.

Margins remain intact though, according to Iowa State’s model:

Corn’s continued slide has helped bolster margins:

Natural gas has offered a nice assist as well, down another 5.2% today hitting its lowest level since June of 2020.

March futures are half of their price just three months ago as abnormally warm temps have obliterated demand in recent weeks.

HOLD THAT THOUGHT…

Blend baby, blend

Conversely, as of yesterday, gasoline futures had rallied 20 cents in the first two weeks of February while ethanol fell 5 cents - sending gasoline’s premium over ethanol north of 80 cents - a six-month high.

This historically high premium of gas over ethanol continues to encourage strong blend rates, further supporting ethanol demand.

This also means we are kicking out plenty of D6 RINS which if you are familiar with that market (D4 too)… that doesn’t bode well for the current saturated state of the biomass-based diesel market.

Back to natural gas:

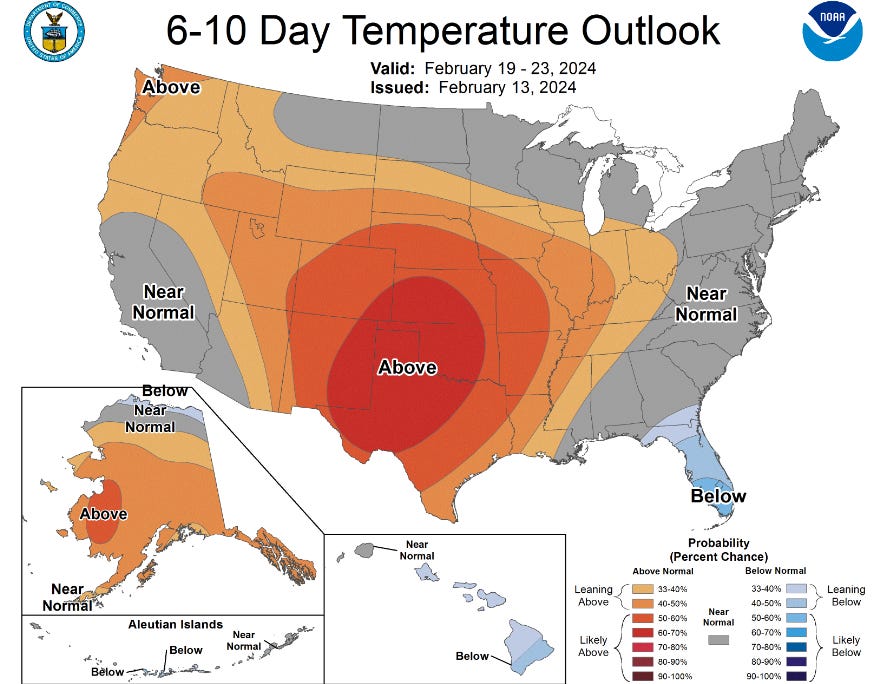

February has been HOT, HOT, HOT!

In fact, it has been one for the record books:

And the trend looks to continue…

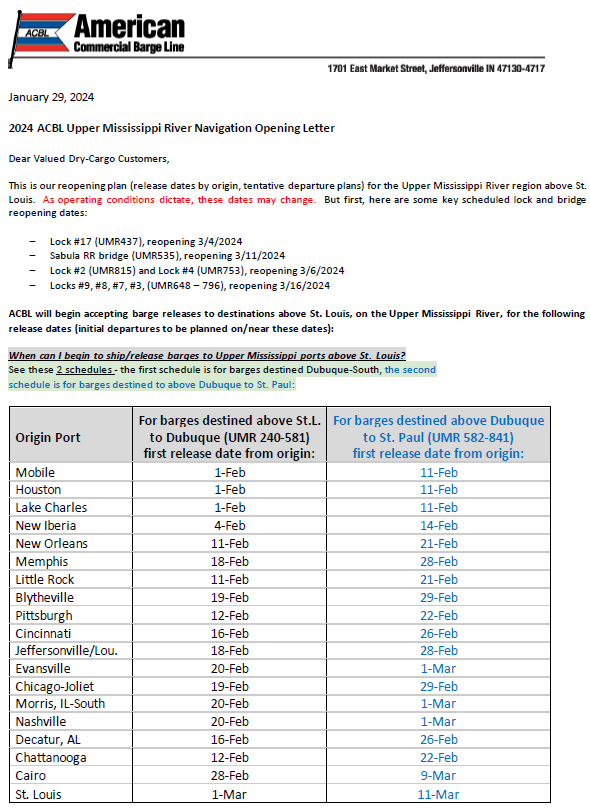

It’s warm enough that the Upper Mississippi River is opening a few weeks earlier than usual:

…which doesn’t bode well for corn as we have already been riding the front seat of the struggle bus with burdensome supplies outstripping demand.

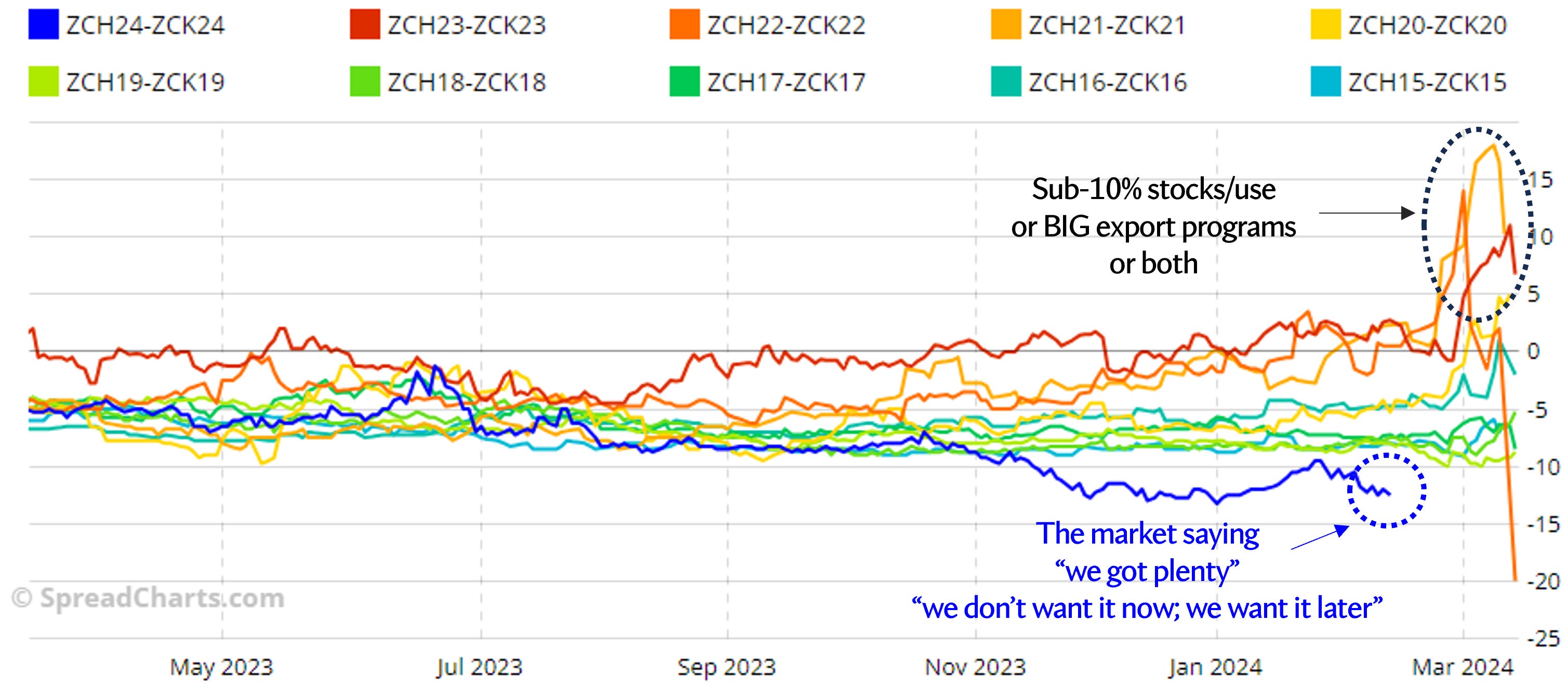

The Breakup.

The March-May corn spread continues to tick wider as the H has no friends heading into the end of the month (i.e. time to set futures on those basis contracts or roll).

H/K has been on a downhill slide for months, except for its brief run at a 9-cent carry as sub-zero temps froze cash grain movement across the heart of the Belt in mid-January, literally.

But what does this mean if the H/K continues to leak lower?

For those unfamiliar: March corn futures minus May corn futures = the spread

CH24 4.24-1/4c - CK24 4.37-1/4c = -13c aka 13-cent carry

The ‘carry’ portion of that means that May is higher than March - the market is paying you to carry those bushels.

Back to the question:

This means we are in the type of environment where basis contracts will kick your a**.

(Because if you are rolling a basis contract, you get to eat that 13-carry - aka your +20H turns into a +7K… kicking the can down the road, hoping and praying for a rally)

Are you listening, Mr. Perpetual Roller?

Today’s carry in corn is a stark contrast of the past ~3 years, where the inverse lived on forever (nearby contract was always higher than the next month).

Today, the market is saying “we don’t want your bushels now” and it is willing to take whatever means necessary to slow the flow.

A Complicated Relationship

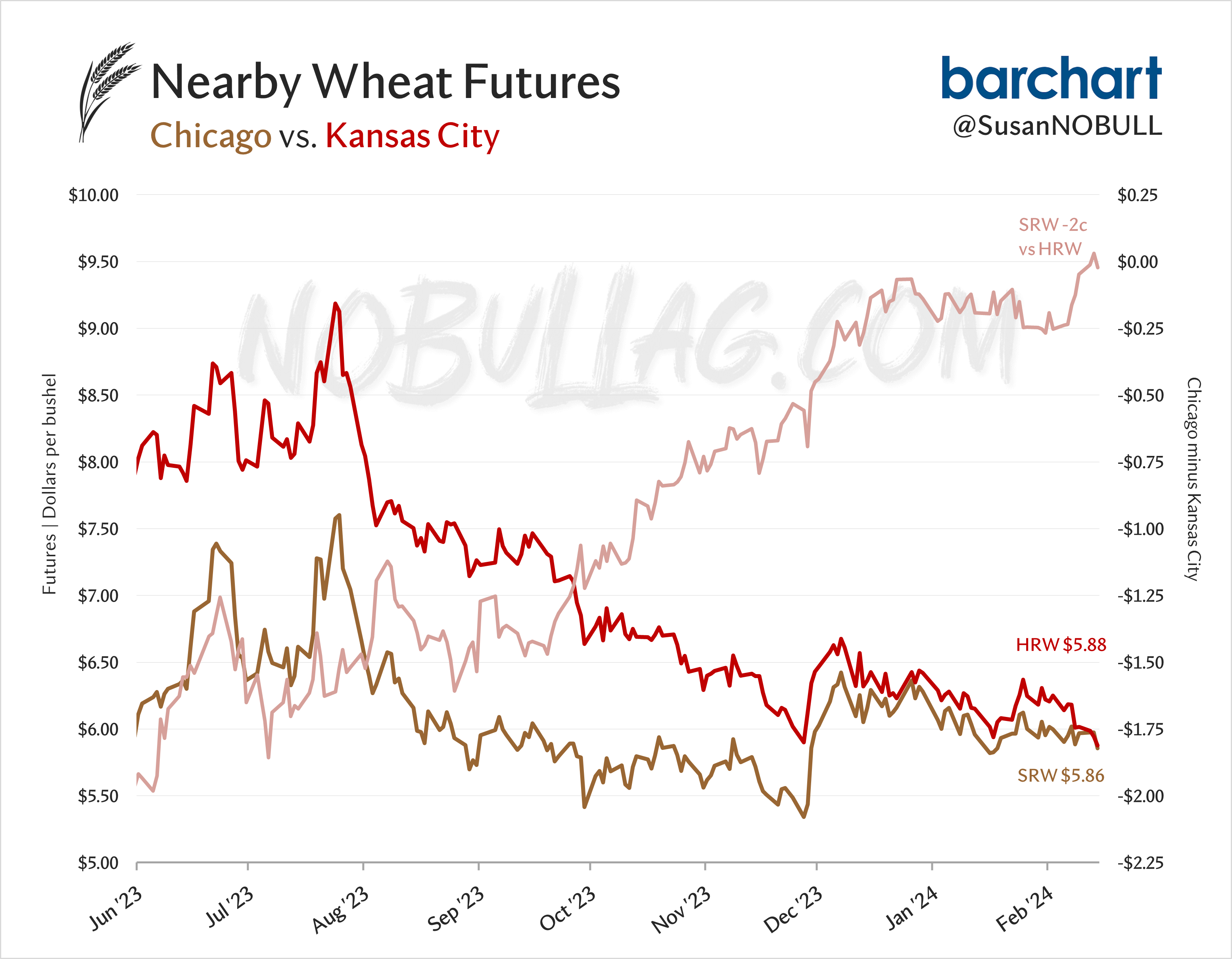

One thing that isn’t helping corn is wheat’s slow grind lower as the U.S. remains uncompetitive with cheap and abundant Black Sea supplies.

As a result we are seeing hard red wheat futures’ premium vs soft red wheat erode as a weak Russian market wreaks havoc on the KC board.

The weakness in KC is happening at the same time exporters are attempting to ship YUGE soft red wheat commitments to China, keeping Chicago futures firm and causing the H/K SRW spread to work its way into an inverse.

Recall we just had a lesson on a carry - here is the opposite, where the Chicago wheat market is saying, “I need all the wheat and I needed it yesterday”:

Alright - “yesterday” is a bit of an exaggeration, but you get my point. For those of you holding onto old crop wheat - HERE IS YOUR SIGN.

It never fails - what I intend to cover in an update and what I actually cover end up being two very different things.

Take today for instance - I meant to hit on census exports, updated feedstock usage in biomass-based diesels, China’s declining population and all sorts of other random stuff, yet I went skipping down a different path entirely.

At the end of the day it is all about the journey and the lessons we learn along the way.

No one likes down days… no one likes bear markets… but we must play with the hand we have been dealt and the only way we avoid repeating our prior mistakes is treating every single whoopsie/failure/F-up as a learning (and growing) opportunity.

For those of you who are on the free version - I hope you have enjoyed this extended free peek at what an upgrade to paid looks like. Click below to subscribe for two full updates each week.

Keep reading with a 7-day free trial

Subscribe to No Bull to keep reading this post and get 7 days of free access to the full post archives.