What’s HOT & What’s NOT

GREETings

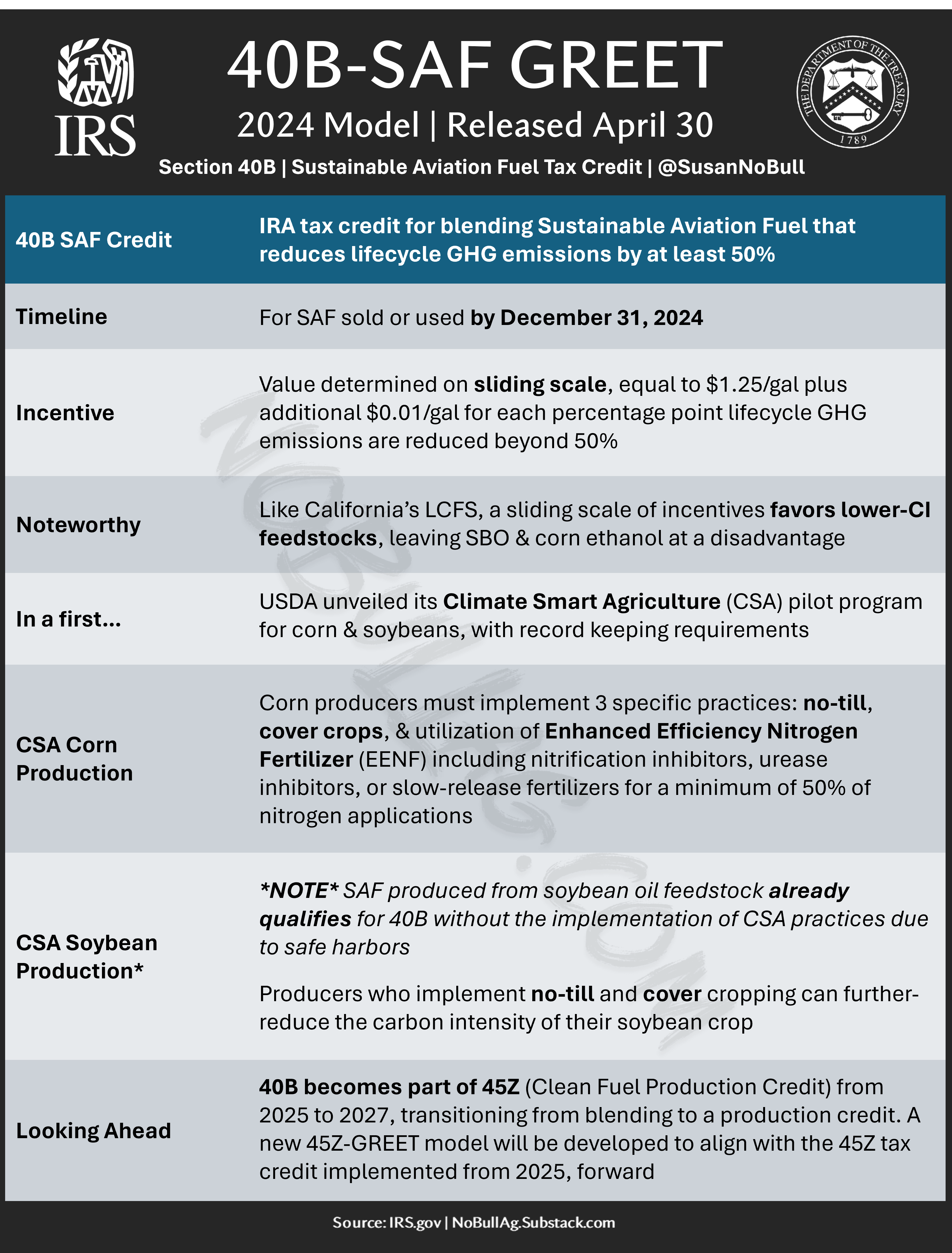

After a tremendous amount of buildup heading into the GREET release (IRS guidance on the who/what/when/where/hows of tax credits for sustainable aviation fuel production provided by the Inflation Reduction Act)…

…Tuesday’s announcement felt like this:

In fact, while important, it seems a bit futile for balance of 2024 as the announcement includes a USDA pilot program to encourage the use of ‘Climate Smart Agriculture’ practices, including no-till, cover crops, and enhanced efficiency fertilizer (corn).

Someone forgot to let the Treasury Department know we are mid-planting season which leaves little opportunity for many producers to change their farming practices for the 2024 crop year as this provision ends on December 31, not to fail to mention the difficulties for biofuel producers to develop last-minute buying programs based on the new 40B-SAF GREET guidelines.

Nevertheless, here is what you need to know about Tuesday’s release:

(updated to add note regarding soybean oil/safe harbors)

Going forward, 40B becomes a part of the 45Z Clean Fuel Production credit, effective January 1, 2025. We likely see the requirements outlined above for 40B bleed over into the modeling for 45Z in future months.

Stay tuned!

A mixed bag

Also Tuesday, EIA released February’s Monthly Biofuels Capacity and Feedstocks Update.

Biodiesel production capacity declined 89mgal, dropping annual biodiesel production capacity below 2 billion gallons per year for the first time since 2011 (assuming this is due to Chevron Renewable Energy’s March announcement of the permanent closure of two plants (IA & WI) due to poor market conditions).

While renewable diesel production capacity didn’t increase (holding steady at 3.86 billion gallons for a fifth month), its growth the past few years is staggering.

Since February 2021, renewable diesel production capacity has grown almost 350% while biodiesel capacity has declined 18% during that same time.

Collectively, biomass-based diesel production capacity has increased 78% the past three years - all on the back of a boom in renewable diesel demand.

Yeow.

Before you start doing cartwheels, let’s hit on the not-so-HOT part of EIA’s release - feedstock data.

While we continue to use copious amounts of soybean oil in biomass-based diesel production - growth has stalled and showed sharp declines in February.

Soybean oil use by weight fell to a 14-month low at 888 million pounds - the first sub-900mlb month since late 2022!

To add insult to injury, soybean oil’s percentage-share of all feedstocks dropped to another record low of 30.8%.

SBO: Not on an island

Overall feedstock demand declined in February too.

Keep reading with a 7-day free trial

Subscribe to No Bull to keep reading this post and get 7 days of free access to the full post archives.