For a printable recap, click HERE.

Corn

As expected USDA raised corn for ethanol and feed/residual demand (this comes on the back of lower-than-expected March 1 stocks. Each were increased 25 million bushels, reducing carryout by 50 million bushels at 2.122 billion.

Not only does today’s reduction give us the lowest projected 2023/24 ending stocks since October, but that 50 million bushels is important as it’s disappearance also reduces new crop carry-in by an equal amount.

Important to note USDA also reduced the current-year farm price 5 cents to $4.70.

Now, keeping that in mind, look at 2023/24 ending stocks (red) relative to last year way down there, sub-1.5bbu (black). Last year’s final farm price was $6.54. That ~760mbu year-on-year increase in carryout is why there is a ~$1.85 per bushel difference in price.

Finally - check out the rough estimate for 2024/25 carryout in blue, then refer back to the paragraph above re price and then remember that USDA’s March acreage estimate of 90.0 million is likely the lowest area print we see (barring a weather catastrophe) BUT we are stuck with it until proved otherwise on June 28.

My point is - this isn’t a $6+ market. It probably isn’t a $5.50 market either.

Manage risk accordingly, my friends.

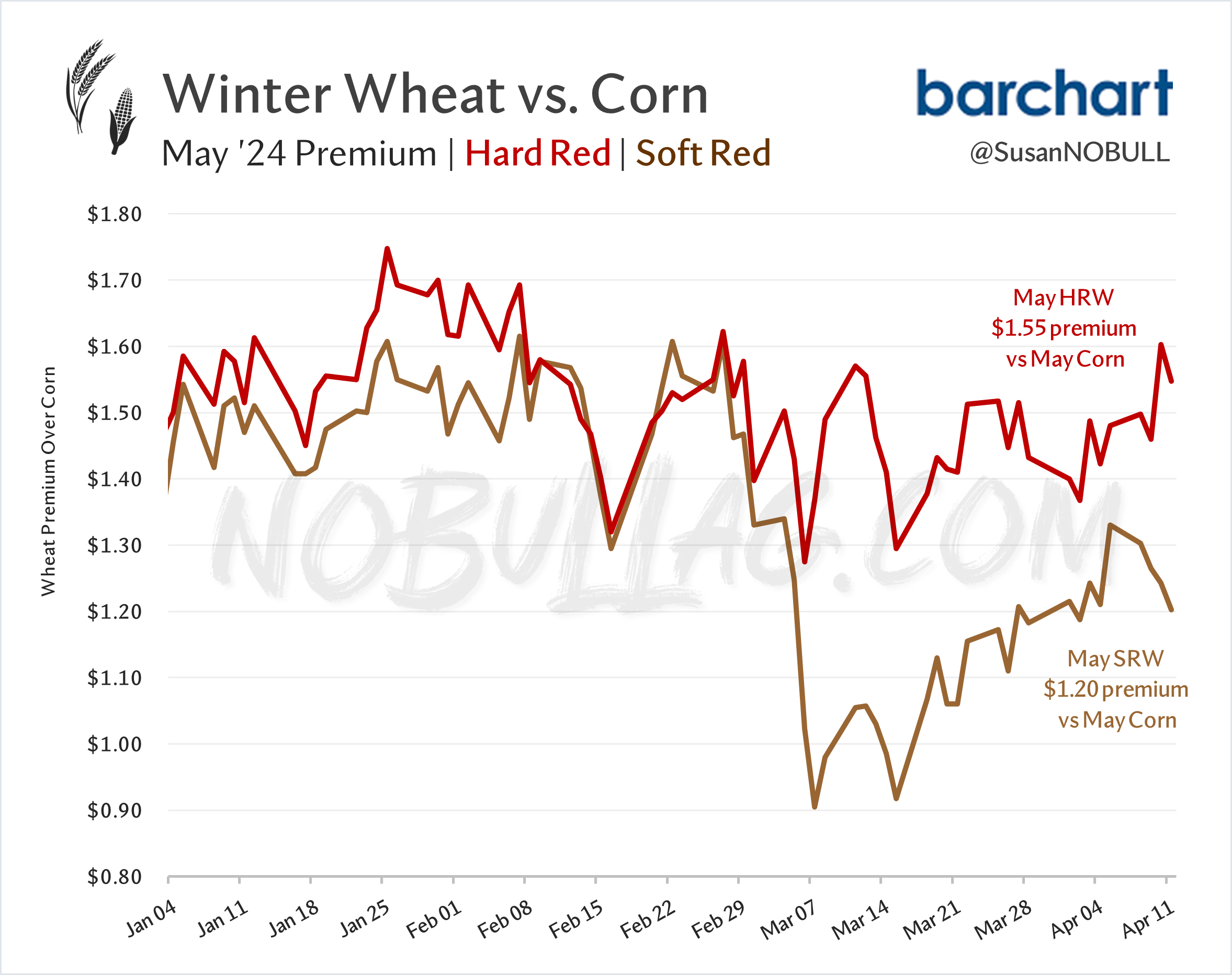

Even with the stocks reduction, corn is trading lower… likely with a little help from wheat which is seeing some double-digit losses itself.

I used this one over the weekend but I want to show it again today, with this week’s price action. This relationship is worth keeping an eye on given wheat and corn’s relationships as feedgrains.

In world changes, Argentina’s crop was reduced 1mmt to 55mmt as leafhoppers have been spreading Spiroplasma bacteria which causes stunt disease.

Keep reading with a 7-day free trial

Subscribe to No Bull to keep reading this post and get 7 days of free access to the full post archives.