Oh, the excitement!

To start things off today, I have a few exciting tidbits to share:

I made my Barchart debut last week! I have been a big fan of their site (and their app in particular) for years. I am thrilled that they asked me to be a contributor and truly grateful for the opportunity.

My distribution list crossed the 1,000 member threshold today. Most of you are still only receiving the condensed, freebie version each Thursday, but hey - you gotta start somewhere!

To celebrate the occasion ALL subscribers (both free and paid) will receive the full version of today’s NO BULL. Yes, this is to encourage you to subscribe!

And last, but not least….

I am so excited this pumpkin is DONE! Four days and a mild case of carpal tunnel later, we have the 8RX John Deere Tripp requested.

We had to start with the largest pumpkin he could find…

Heaven forbid he pick a simple design…

That’s alright. It turned out pretty cool and Tripp has a big smile on this face, which was the goal.

Thank goodness this only happens once a year, otherwise I would need to invest in a wrist brace!

Alright, let’s get down to business.

This week, we are doing another round of Ask the Experts. I did this about six weeks ago and it was so popular, I decided to do it again.

You can check out early-September’s Ask the Experts HERE, featuring one-on-ones with Jim @theLandTalker Rothermich, CGB AgriFinancial’s Alan Singleton, Brian and Blake from Heartland Barge & Companies, and Eric Kelly with AmmPower (GREEN anhydrous ammonia).

Carter! We first met several months back and reconnected after (rumor has it) a few Bloomberg hosts used my last round of Ask the Experts to prep for interviewing you about farmland on live TV!

AcreTrader is growing like a weed. Fill everyone in on what AcreTrader is all about.

We are an online farmland investment company offering individuals the opportunity to buy shares of high-quality, individual U.S. farms while also offering producers the chance to grow their business as partners.

I understand the value of farmland as a long-term investment, but many outside of rural America do not.

What does AcreTrader do for the investor and why would an individual want to put money into farmland versus some of the more traditional investment vehicles?

Farmland has historically yielded consistent returns and outperformed during volatile market conditions. For example gold, long considered THE inflation hedge, has performed terribly this year, returning -6.88% over the last 12 mos. Farmland, inversely, has a positive spread to CPI going back to 1970 with 0.65 R2 to CPI in that same time period (compared to gold at 0.28).

In fact, research from Nuveen, the $1.3 trillion investment manager of TIAA, has shown that adding 2-5% of a portfolio to farmland and/or timberland can improve a portfolio's overall returns and, at the same time, reduce risk.

Tell me a bit about the investing process. Is there a minimum investment amount and what does your typical investor look like?

The investment minimum is $10,000 to $20,000, depending on the farm.

We currently have thousands of investors, all of which are legal U.S. residents. A large portion of our investors hail from rural areas as that demographic tends to understand the value of land but may not be able to spend $1 million or more on a farm. This is where we can provide them with that opportunity without breaking the bank.

We also see a lot of farmers investing in land with us as they seek to diversify their farmland portfolio, be it investing in another area of the country or seeking out investments in different types of crops. We have everything from your traditional row crops to permanent crops like orchards, potatoes, avocados, and even timberland.

How many acres do you currently have under management and what type of growth are you expecting in the next year?

AcreTrader is coming up on its 5th anniversary. One year ago, we had 50 employees. Today, we have 150, so we have seen tremendous growth.

Our platform has had hundreds of millions of dollars invested, encompassing well over 30,000 acres with more than 100 producers. We even have a few large operations in Australia.

What about the process for producers that are looking to expand their operation? How long are lease terms? How are cash rent levels determined?

Are there ownership opportunities if the ground is up for sale (farmer tenants often rent a farm waiting on the opportunity to buy it)?

Often-times farmers come to us with a farm that is up for sale as they know their local area better than anyone. For instance, a producer’s current landlord might be selling the farm or a neighboring farmer may be retiring, but the producer doesn’t have the means to purchase it.

This is where AcreTrader steps in. We can help purchase the farm via our fractional investment model and then work with the producer to renew the lease, so they can continue to farm those acres. Plus, we often do improvement projects on newly purchased farms. We raise capital through investors to cover things like ditches in the Delta or tiling projects in the Midwest.

Farms are being bought and sold regardless. Our goal is to partner with farmers to grow their operation. We are the alternative way to scale your operation.

Others have tried to revolutionize the cash rent scene before… and it turned into a PR nightmare. What makes AcreTrader different?

We understand the real value from investing in farmland is the long-term price appreciation, therefore we are not going to grind for that last $20 an acre on rent.

Plain and simple, we are here to help producers grow their operations. We understand tenant relationships are personal in nature and we intend to keep them that way.

What is the best way for producers to get started with AcreTrader?

If you are a farmer, visit the For Farmers section of our website. Better yet, call us at 1-888-958-1470 and we will help you get started in the process.

We have an entire team of agricultural experts located here in Arkansas dedicated to working with farmers.

Potential investors can visit us at AcreTrader.com for more information.

You also have a VERY cool (and free) mapping website that everyone should check out.

Tell me more about Acres.co and how it stands out from dozens of other mapping platforms that are out there, both for free and as a subscription service.

Acres.co is our new, powerful mapping tool. We want to make evaluating land less burdensome and opaque. Our free platform even outperforms paid land apps because we offer better up-to-date information with confidence.

We have land ownership information, soil mapping, vegetative health, crop history, and even land sale datas. Without Acres, evaluating a single property can take about half a day or more, and with Acres it’s pulled together in one place in minutes.

You have the ability to customize maps and there are reporting features – all conveniently packaged on the Acres.co website or our app that is available both for Apple and Android devices.

We have a great, new feature coming soon that gives us the ability to display land that is for sale too. We’re excited about how Acres will change the game for land owners and investors and love bringing both producers and investors value with this mapping platform!

Alright Carter, one last thing: what do you consider to be the coolest farm in AcreTrader’s investment portfolio?

Now, that’s hard to say. One of the most interesting is a timber property in Arkansas where oak is harvested to make whiskey barrels. We also have a hand in a few organic operations as well as a farm in Michigan that grows vegetables for Gerber baby food.

And then the Australian properties certainly are top of mind. Those serve as a great example of things to come to AcreTrader as we expand our reach not only here in the United States, but abroad.

Thanks, Carter! You have exciting things happening and I look forward to speaking with you again soon.

Hey Dan! First off, tell me a bit about InterMat.

We are a consulting firm specializing in the commercial, financial, engineering, and operational aspects of Intermodal rail, marine, and inland terminal industries. Our team is comprised of recognized industry experts in bulk and breakbulk material handing systems, port and rail facility design and operations, and multi-modla logistics management. Our main office is located in Metairie, Louisiana in the heart of the Gulf.

In last week’s NO BULL I made a few comments inferring that the current low water situation on the Mississippi could really turn into a mess this winter. You emailed me in response. Can you share a few of those thoughts?

Sure. Based on the current light loadings, tow restrictions, water conditions and forecast, along with the pending grain hangover coupled with redistributed global fertilizer trade, we have only begun the mess that will be river transportation over the next 12 months.

If the above factors hold into early 2023, we see Northbound fertilizer trading at a significant premium due to capacity constraints which will only increase the wholesale/retail cost. These will likely be compounded by a lack of landside storage.

Uh oh, there are a few ears that perked up when they heard the words “fertilizer” and “premium” together in the same sentence.

Can you give us a bit more detail on how you see the current low water conditions impacting fertilizer availability and subsequently pricing in the coming months?

As with many things, there is a domino effect. Southbound traffic has been a mess, making transit times slow and leaving barges stuck in some areas either due to closures or draft restrictions.

When southbound barges are not hitting the Gulf in a timely manner, it delays vessel unloading and ultimately reduces the number of empty barges available to load products to head back north.

Without adequate empties on hand, the offloading of vessels carrying imported fertilizer or other raw materials can be delayed, which has a ripple effect throughout the system.

Fertilizer imports tend to ramp up in late December, extending through January and later. The writing is on the wall – we have serious capacity constraints that will ultimately drive transportation costs higher.

(This is an old video of mine: fertilizer vessel being offloaded mid-stream in the Gulf region. Apparently I didn’t manage to catch an empty barge being loaded while taking the footage, coincidentally the same situation Dan is describing)

I feel like my grandma saying this, but the price of everything is so high anymore. We have all seen what happens to corn and soybean basis when barge freight costs rise, but what else has an impact on overall transportation costs?

We are seeing barge demurrage increasing. Demurrage are added costs incurred if a barge is not loaded or unloaded within a certain time. Higher labor costs, a higher inventory carrying cost due to the current cost of capital, and the fact fuel has tripled in price all effect the system.

Plus, vessel demurrage can incur costs up to $50,000 a day if the vessel is not unloaded on time. Think about the implications if you are stuck waiting on empty barges to offload a fertilizer vessel. That gets expensive quickly.

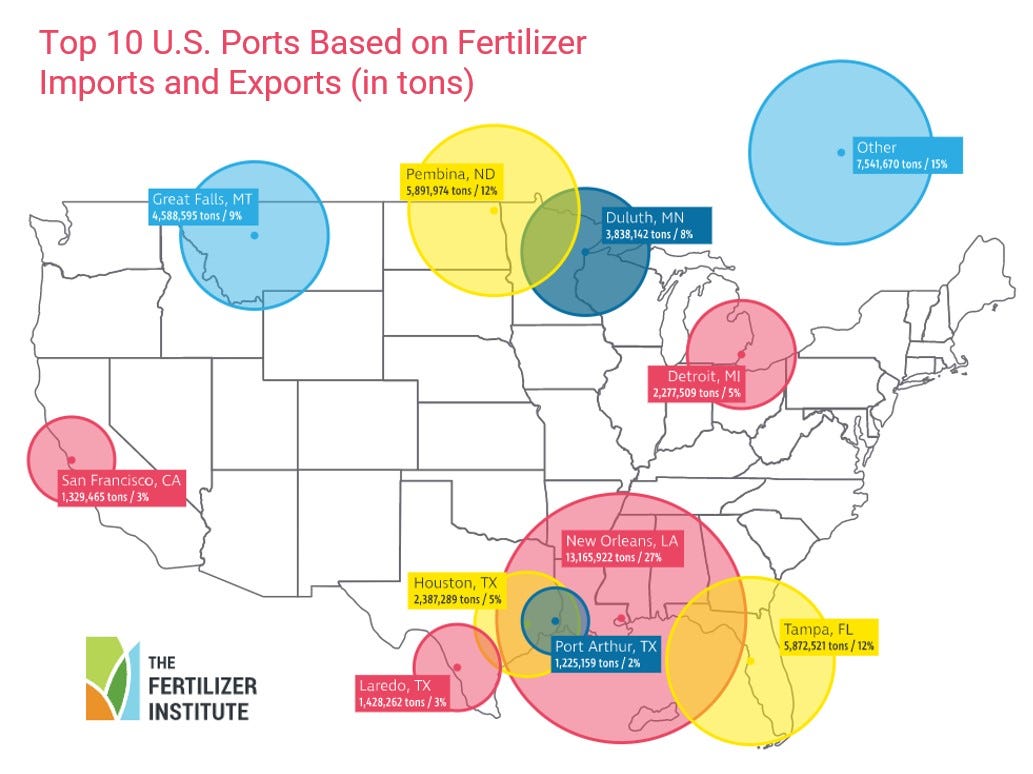

The Gulf is the largest fertilizer-importing region in the country, more than double the annual import tonnage of any other US port. Those imports rely on the inland waterways system for distribution and do not have the option of rail. We need more water in the system.

Vessel demurrage is wild! I have always been fascinated with all things related to vessels as the numbers are just so big. Ships that are a quarter mile long and can hold more than two million bushels of grain are just mind-boggling.

Any last thoughts before we wrap it up?

Pretty unprecedented times on the river, so until something changes its going to take the lead on lot of shippers’ minds. Couple that with railroads that are still figuring out how to move cars and the potential for a lingering strike, we live in interesting times.

Unfortunately, all of these challenges and added expenses trickle down to the end user, for both importing countries buying US grain or US farmers buying fertilizer.

Thanks for your insight, Dan!

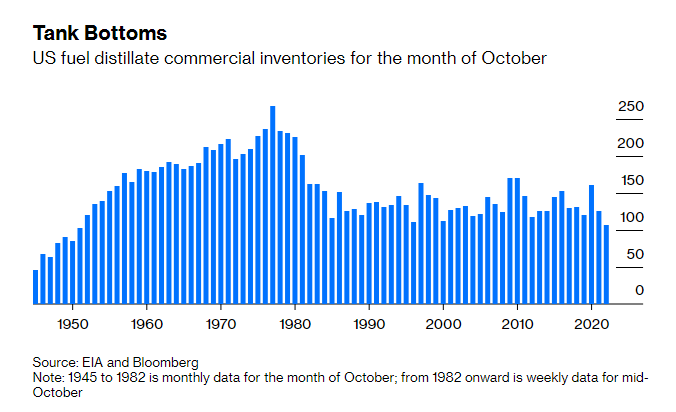

Dieselgate 2022

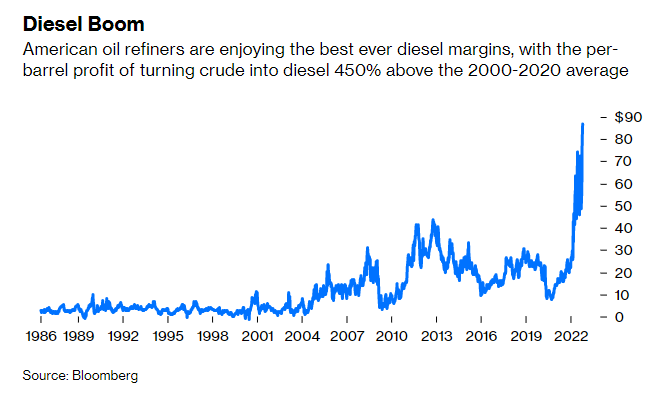

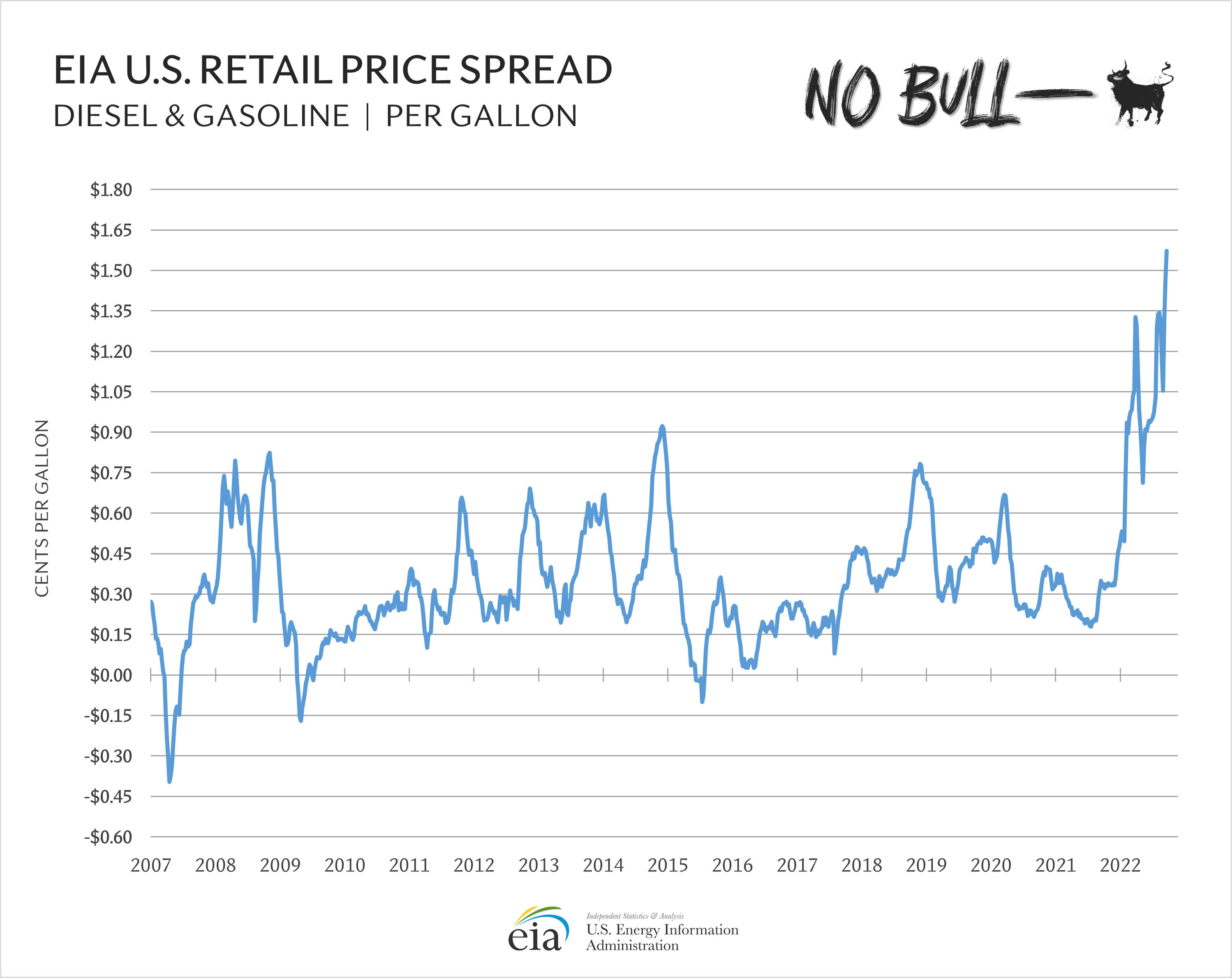

As you know, diesel is on fire with average US weekly retail prices eclipsing $5 for the first time in history this past March, and only dipping below that mark six times in the months since.

According to EIA, the average on-highway diesel price in the US is $5.34 per gallon, a whopping $1.63 per gallon higher than one year ago. To top it off that compares with retail gasoline prices at $3.77 per gallon, only 40 cents higher than one year ago.

These wild prices and wide price gap with gasoline bring about many questions like why is this happening? and when will things get back to some sort of normal?

To answer these questions, I phoned a friend who put me in touch with two energy experts with over 50 years of oil industry experience, combined. The kicker is our experts asked to remain anonymous, which is fine by me because I really appreciate them taking the time to answer my questions and their willingness to let me share that insight with you.

Mystery men, how in the world did we get to this point with $5+ diesel becoming the norm for more than six months?

It was the perfect storm of Covid, U.S. Administrations (including past and present, plus the RFS) a push for green initiatives, in our opinion and a lack of investment into refining capacity.

When Covid hit, margins went into the gutter and refineries shut down. Many of those were never brought back into operation. Right now, there are only three in operation on the East Coast. One of which only recently came back online, capitalizing on the massive increase in refining margins we have seen in recent months.

The country (and world, for that matter) is undoubtedly headed in a greener direction, which has disincentivized refiners from further investments and maintenance. This, plus throw in a war where the second-largest oil producer and exporter in the world suddenly became public enemy #1 and you have a massive problem that disrupts global tradeflows and keeps energy prices elevated for a prolonged period of time.

Tell us a bit more about those disruptions. This just shuffles the deck a bit, right?

Consumers are trying to get away from Russian oil, which shifts around how the supply chain works. Right now, you see a lot of Russian oil going to China or India, where OPEC would have usually supplied their needs.

Freight markets are going crazy because it isn’t the efficient way to transport fuel from the Middle East up to Europe. It is efficient to go from the Middle East to India or Asia, and likewise from Russia to Europe. It is a much shorter trip than going thousands of miles around to China or India.

S&P Global has a fantastic Global Oil Flow tracker HERE.

Getting back to what I will term ‘Dieselgate 2022’ – what can help us return to some level of normalcy?

First of all, remember that diesel is a global commodity and gasoline is a US commodity as there are a lot more gas-powered vehicles here in the US versus abroad. We here in the US are the driver for gasoline demand and when prices got really high this summer, we saw demand fall off. Americans will cancel their vacations or cut back on driving.

Diesel, on the other hand, doesn’t see fast demand destruction. It is a commercial fuel and the demand is stickier. You have to see a business slowdown or major recession to truly tamp down demand.

Diesel is a commodity that is short across the world and until we see a notable decline in global business activity slowing demand, I would expect to see prices remain high.

The quick way to get prices back down is a recession. End of story.

Thank you so much to my energy expert Mystery Men!

Thanks to Carter, Dan, and my Mystery Men for giving us a little insight this week.

Plus, thanks to my long-time readers and the newcomers. Exciting things are up ahead and thrilled you can come along for the ride.

If you are interested in receiving the full NO BULL every Thursday, in addition to The Tuesday HOT TAKE (grain-focused) and The Weekender (grain with a sprinkling of insights into Agriculture that should be on your radar), you can subscribe below.