No Bull | It's All About Perspective

February 9

Meet Genevieve’s new plush possum, fresh off the shelf at Bass Pro earlier this week.

You might be a redneck if…

From her perspective though, it is a mouse… a “mouse” that must accompany her everywhere, otherwise I am stuck hearing, “my mouse! my mouse!”

Final Thoughts are coming first today:

It's All About Perspective

Looking at something from a slightly different angle can change its meaning or its impactfulness, in a big way.

In fact, I view perspective with so much importance that I had considered it as a name for this weekly wire - before settling on the name No Bull a few years back.

Let’s face it, there are a million variables that move and shape markets every day.

In my last fifteen years or so of observations the only constant has been our reluctancy to adjust accordingly.

The problem here in the United States is we have spent far too much time arguing USDA or worrying about missing the high that we often lose sight of the things that actually matter.

#1) Farming is a business (and should be operated as such). Yes, I am talking to you, Mr. Gambling Grain Hoarder

and #2) the US has turned into a residual supplier for beans and now corn, as well.

What’s that mean? Residual means we are now #2… or #3… as world buyers secure their import needs from other origins before purchasing pricey US supplies.

So - this week’s update might chap your backside a bit but you are guaranteed to walk away with a slightly different perspective.

Full-Steam Ahead

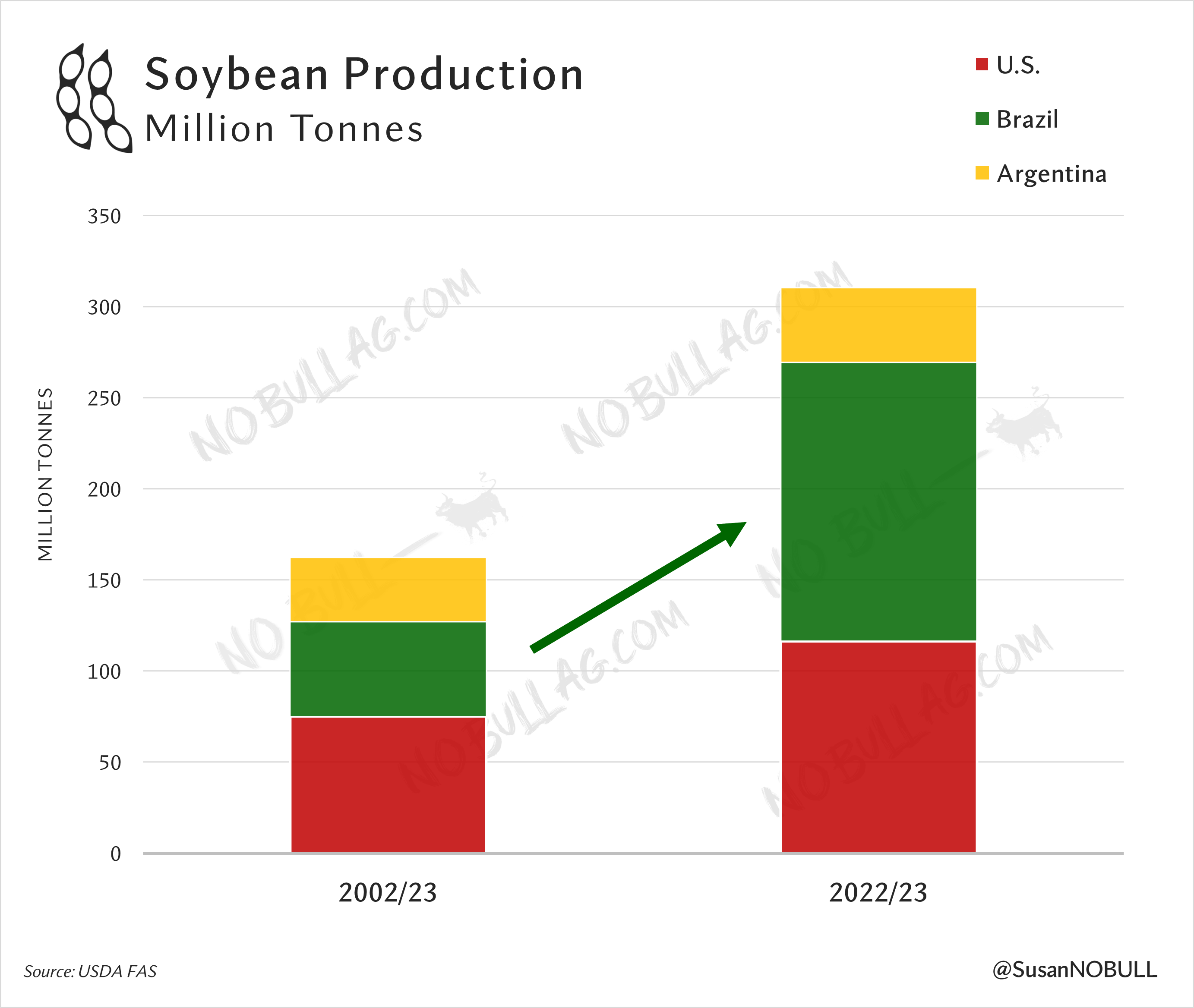

It isn’t new news that Brazil has been in major expansion mode for the past several years.

I think we all know they have blown right by us but the numbers still blow my mind, especially when placed beside US statistics.

Brazil will harvest 107.2 million of beans in 2023 vs the US at 86.3 million acres (that’s a difference the size of IL & IA’s 2022 harvested acres combined)

At 3.53 mt/Ha, Brazil is set to see 52.5 bushels per acre with this crop vs 2022 US yield of 49.5. Mood killer!

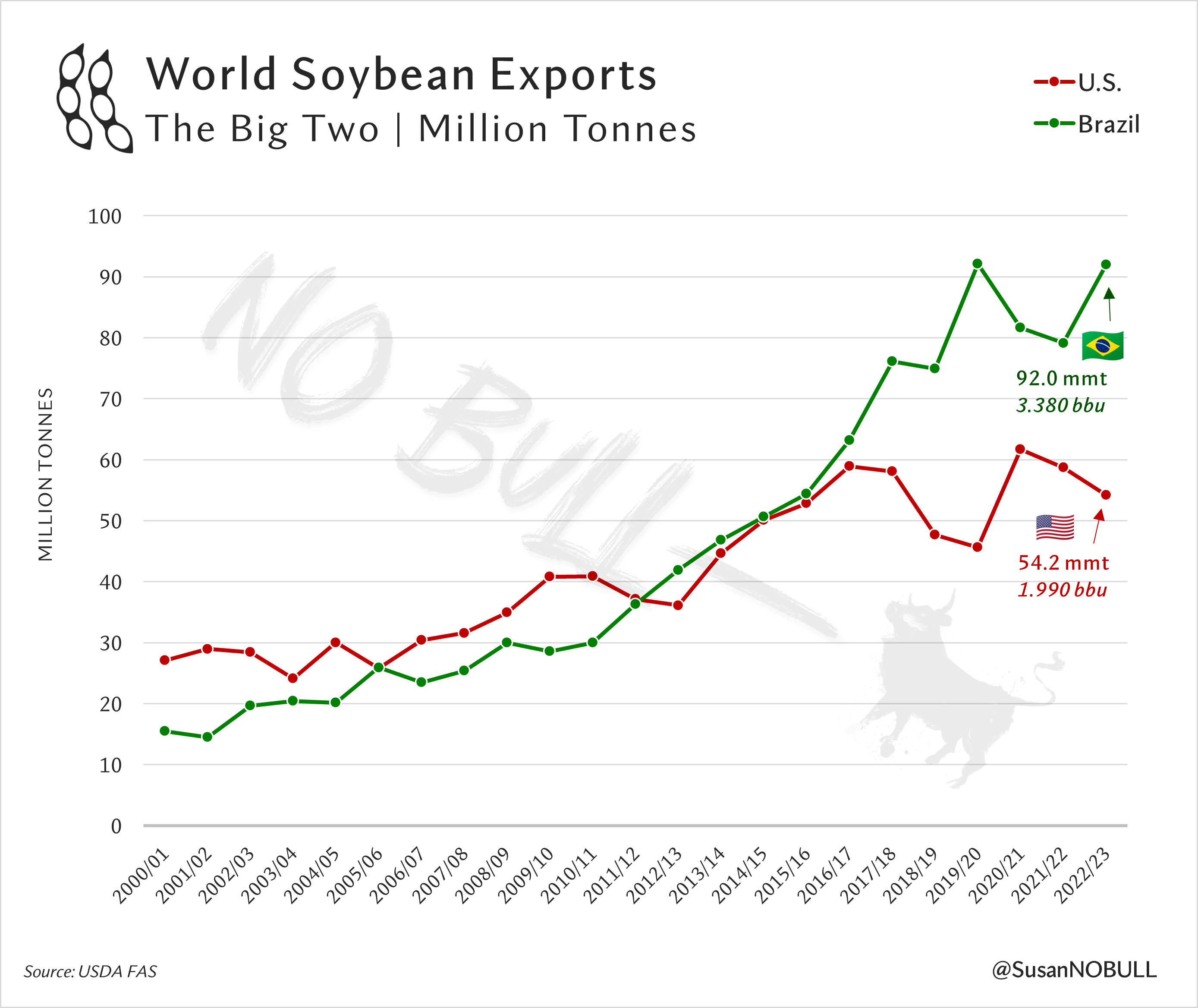

Brazil’s exports are expected to be a record 92mmt in 2022/23 (3.380 bil bu), 70% larger than USDA’s current US export estimate of 1.990 billion bushels

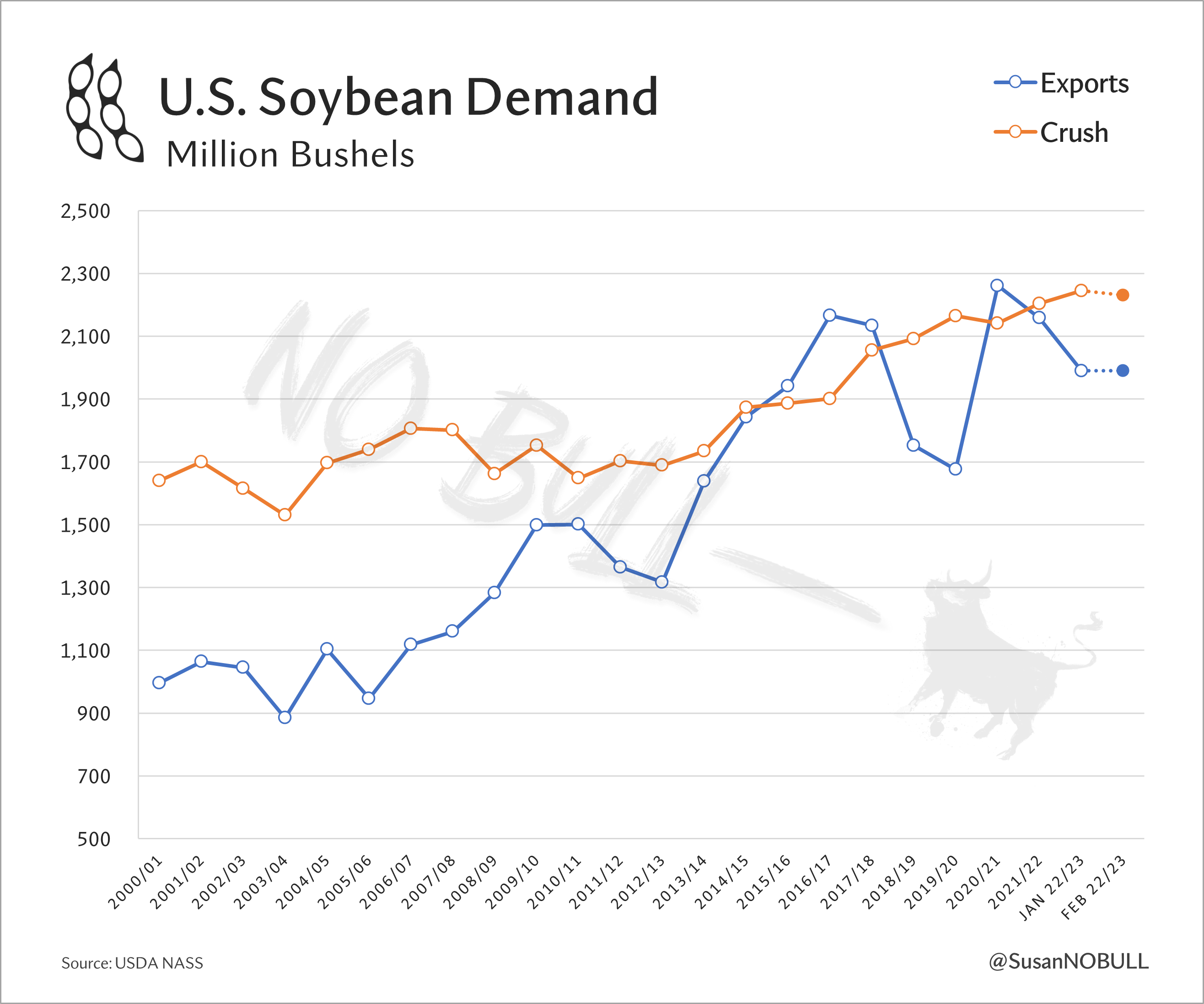

Brazilian crush is also expected to be a record at 52.75mmt which falls about 300 million bushels short of the record 2.230 billion bushels the US will crush this year

This is the one spot Brazil won’t catch the US, as the Renewable Diesel boom will keep more bushels here domestically to crushed, reducing our exportable supplies as capacity grows

Dethroned

All hail King Corn, but the bad news is the US has officially lost its crown.

In a first, Brazil is expected to export more corn than the United States in 2022/23, edging us out by 40 million bushels as USDA raised their export estimate to a record 50mmt in Wednesday’s report.

Technically, Brazil did ship more bushels than us in 2012, but that was an anomaly thanks to drought.

The past several months have ushered in a wave of changes in corn market dynamics as US bushels have spent months as the most expensive in the world and China opened its doors to Brazilian corn imports for the first time in history.

See that spike in the green line below? Messy river logistics caused domestic transportation costs to skyrocket… added expenses that were ultimately passed on to the world buyer (who clearly didn’t buy).

US bushels were $1.50 to nearly $2.00 more expensive than our Southern Hemisphere rivals at one point this past fall as the US dollar’s run to 114 only compounded a struggling river system’s effects.

The problem is far greater than this year alone though, as the US accounted for two-thirds of world corn exports in the early 2000s, but our share has has dwindled down to less than one-third of world exports today.

The bad thing is, the US has been losing marketshare to a crop that isn’t even a full season crop!

Now, before you get angry and click unsubscribe, there is a greater point to be had - and for those reading the free version, you have reached the end of the road ;)

Keep reading with a 7-day free trial

Subscribe to No Bull to keep reading this post and get 7 days of free access to the full post archives.