Hurry up and get dirty was the theme last weekend as dry weather turned the pumpkin patch into the Dust Bowl.

By the time I realized what she was doing, it was too late. She just kept saying, “beach! beach!”

Tripp did not get nearly as dirty, but I did turnaround once to find him up IN the apple tree (hard to tell in the pic, but trust me - he is off the ground).

$97 later we walked away with four pumpkins and a bag of apples.

An Epic Wait

Last Friday, ACBL reported staggering figures related to the on and off closures of the Mississippi River near Stack Island, MS:

A total of 185 boats with 2,892 barges stuck waiting to transit the area - the largest closure ever recorded.

I am not sure what you may imagine a river traffic jam looks like but it isn’t just a big barge parking lot.

Backups extend for miles as line boats are forced to idle along the bank.

While a little blurry, a picture is worth a thousand words boats. Boats, boats, and more boats waiting to resume their journey.

Thanks to Jason Graddy for these images and the video below.

Jason works aboard the Miss Marley which spent the better part of last week idling north of Stack Island. This video was taken as the Miss Marley transited the problem area:

Notice rock piles? Those are dikes that would normally be several feet underwater.

Dikes (or wing dams) are built to redirect water and manage sediment, making the channel more navigable.

Low water has left plenty of dikes (horseshoes) visible from the air too as seen in this picture taken last weekend:

Hurry up and wait TO DELIVER

*Disclaimer - these are rough calcs just to illustrate a larger point. While the information is accurate, I am going to round for ease of discussion*

Ever look at a grain elevator bid sheet and wonder how in the world they arrive at those prices or why there can be such large differences from month to month?

Take Bunge’s river facility in the St. Louis area, for example.

You can sell beans today or wait just over 2 weeks to haul them for 87 cents more.

What gives?

At river facilities, the bid is a direct reflection of what bushels are worth at the Gulf (CIF) and the cost to get them there (barge freight).

So take October delivery soybeans, for instance:

October CIF has been trading somewhere around 210 (aka a +210x basis). Freight in St. Louis last traded near 2200% of tariff (aka $2.60/bu of beans).

+210x at the Gulf - 260c for freight = -50x FOB (aka what it is worth loaded on a barge)

In this example the elevator has about 30 cents of margin to put it through their facility, pay the staff, keep the lights on, etc.

This type of big, fat margin is NOT normal in St. Louis, but in wild times like this elevators want all the breathing room they can get.

A few things to remember:

Every elevator is different. Given today’s wild meme-stock-style freight market they are going to back off bids until forced to follow a competitor higher (or lower).

River facilities tweak both CIF and freight higher and lower depending on their sales, freight positions, and needs. Plus like mentioned above - the competition.

Competition is stiff in large markets like St. Louis. I often refer to it as the “thin margin capital of the world” because it is. Typical margins are a nickel or less.

I will save this discussion for an upcoming post in my new (paid subscriber) weekend edition, but markets like St. Louis are really interesting as elevators can often be considered loss-leaders for huge exporters.

Back to Bunge’s bids. Now that you kind of know the process, here is a breakdown of current values:

There is an 85-cent difference in this example from October to November-delivered soybeans even though October values at the Gulf are 20 cents higher than November.

With freight being nearly $1 more expensive, it absolutely kills the October basis in St. Louis.

Likewise, November beans at the Gulf are worth 35c more than December (X/F spread @10c), but barge freight is so much more expensive for November that it leaves the Dec bid 50c higher after the dust has settled.

And last but definitely not least: if you are in a river market ALWAYS ask for a Last Half November bid. There is a good chance it will pay more than December as you capture some of the November CIF premium but benefit from cheaper freight.

Hurry up and BID!

There was some big bidding happening Monday in Iowa as 55.56 acres went for $1.458 million - $26,250 an acre, marking Iowa’s second sale north of $26,000 in recent months and a new record for the state.

As usual, Jim @theLandTalker Rothermich filled me in on the details:

Bidding started at $17,000 and went up $1,000 an acre to $26,000. There were three bidders remaining at $25,000.

The winning bidder and runner up were both local farmers.

The most interesting thing about this sale is the fact the piece was odd-shaped and has power lines crossing it (yuck). Jim noted there was no influence from development or wind turbine income.

He also mentioned there is a substantial amount of land coming to auction in the next few months and expects more records to fall.

You can read more about Monday’s sale HERE.

Wait a minute… wrong direction!

After five consecutive weeks of retail diesel fuel price declines, we made an about-face this week, up 39 cents at $5.224 - a 12-week high.

Seem like that is a bit of a jump? That is because it is.

This week’s surge is one of the largest one-week increases on record only falling behind a few wild weeks that came immediately after Russia’s invasion of Ukraine.

When compared with gasoline… well, there is no comparison.

Diesel has been on a tear, averaging $1.00 more per gallon than gasoline since the invasion. Today, retail prices are more than $1.30 higher driven by worldwide demand and refinery issues.

I will let EIA’s graphs do the talking:

Nice lil’ bump there.

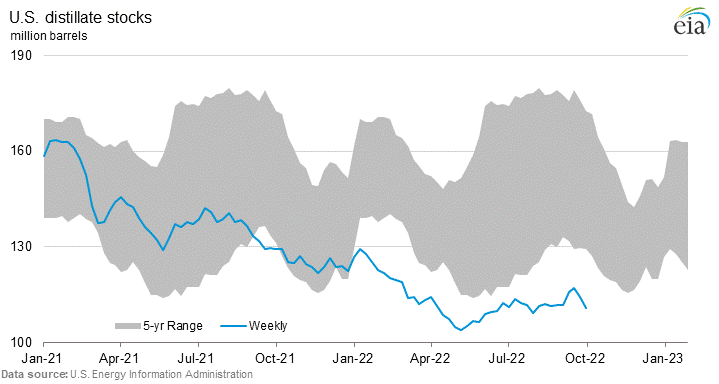

Houston, we have had a continued problem. Distillate stocks hit their lowest levels since May this week.

If you are unfamiliar, distillates include diesel fuels and fuel oils that are used for heating and power generation:

Winter’s a’ comin’

Money talks and BULL—— walks.

Exports of US petroleum products rose to their highest level on record last week - 7.1 million barrels per day.

Funny how that works, isn’t it?

Final Thoughts

Hurry up and wait

I have been desperately waiting for a stretch of normal but clearly it has yet to arrive.

In the short audio recording for consulting clients today I literally gave up.

Between inflation numbers, the dollar, stocks, an impending global recession, a war, a (what’s looking like failing) export corridor, oh and a big WASDE report this week… it becomes a bit difficult to manage.

Whoops - I forgot the fact the Weather Channel referred to the Mississippi River as a “creek” this week.

I am kind of glad I decided to go to three updates a week because I feel like one per week doesn’t give enough time to cover all of the aforementioned hot messes we are juggling on a weekly basis these days.

For tonight, here are a few things I think it is imperative you watch as a producer as harvest drags on:

Be mindful of bid structures. What is Oct vs Nov or even last half Nov? What elevator is still hungry for bushels vs who is not? Do your homework because it pays.

The carry does you no good until you lock it in! If you are filling the family pool with soybeans because the LH Nov bid is $1.25 higher, you better sell it, silly.

For my river guys - diversify your sales a bit. If low water sticks around (which it looks like it will), you are going to be facing slower-than-normal switches, long lines, and the potential for reduced hours. Don’t back yourself into a corner. Spread your sales across multiple elevators and consider ethanol plants or other processors as well.

And lastly re harvest - stay safe. Shortcuts don’t pay.

The next update will be at some point over the weekend. That will be the last of the freebies.

Thanks!