How low can you go?

The river is running dry & the government is digging a hole

October 6, 2022

Welcome to the new NO BULL————

So I am trying this Substack thing and I do not really know what I am doing, so bear with me during this transition.

No matter your subscription status, this week’s update remains the original long-winded FREE version of NO BULL————. Going forward, however, the FREE (aka lite) version will be shortened.

Paid subscribers ($29.50/month or $295/year) will receive the original, full version of NO BULL————, plus two other weekly updates. The two additional updates are TBD but they will be more grain-focused, will include plenty of pictures (because let’s face it - we all like pictures) and will not have filler. There is nothing worse than typing something just to be typing.

Without further ado, click below if you are ready to subscribe to the full NO BULL———— experience:

To quote Travis Tritt, I live ‘where corn don’t grow’.

We took the kids to Elephant Rocks State Park recently, enjoying the nice fall weather.

I love it how the only two kids looking at me are not even mine!

How deep of a hole can you dig?

‘Tis the season to talk about debt, especially for those of you renegotiating rent agreements which have undoubtedly done their best to keep up with inflation. If you thought $600 cash rent was out of the question - think again, because it is happening in central Illinois.

Once you pick your jaw up off of the floor, be prepared to fetch it again with this next number as America's national debt exceeded $31 trillion for the first time earlier this week.

$31,064,646,000 to be exact - that is more than $93,000 of debt for every person in the country.

This mantra of spending more than we collect isn’t new. The bad thing is our debt has grown large enough that it can no longer be ignored, especially as interest rates are on the rise.

Here is a (not so) fun fact: At $31 trillion, we are spending more than $965 million each day on interest ALONE.

Worse yet, with rising rates, interest is set to become the fastest growing part of the federal budget.

Interest expenditures could exceed what the United States spends on national defense by 2029, if interest rates on public debt rise just one percentage point higher than what the CBO has estimated over the next few years.

CBO currently projects the increase in interest payments as debts mount and rates rise will account for 50% of the projected growth in federal debt by 2052.

This is only for illustration purposes because the government is perpetually issuing new debt (no fixed rate here), but imagine that you took out a 30-year mortgage to pay off $31 trillion in debt:

At 7% interest, your monthly payment would be $206.2 billion. Just one year ago, that same monthly payment would have been $130.7 billion at 3% interest. That is an extra $75.5 billion a month in interest costs alone.

The deep hole only gets deeper with rates on the rise.

LOW Emissions

I will let Reuters do the talking:

Oh boy. Never a dull moment with the EPA, the RFS, and Reuters, for that matter.

Here is what we know:

The Renewable Fuel Standard forces oil refiners to blend billions of gallons of biofuels with their gas/diesel each year

This can be accomplished by blending actual gallons of biofuels or buying RINs (paying to stay compliant)

If EPA expands the program to include EVs, these new ‘e-RINs’ would benefit carmakers like Tesla, operators of EV charging networks, & more

The RFS as we know it today, ends December 31, 2022

EPA is set to unveil the 2023 RFS by November 16

Arguing about carbon footprints or who is greener than who is becoming about as common and heated as duking it out with USDA over yields.

Nonetheless, the Renewable Fuels Association has been on the defensive recently after a Reuters ~oh, them again~ article suggested ethanol emissions were higher than that of gasoline.

The Reuters article has since been withdrawn, but you can check out the RFA’s response HERE.

Tired of carbon, emissions, renewables, and ‘green’ talk yet?

Better get used to it because she ain’t going away! Stay tuned.

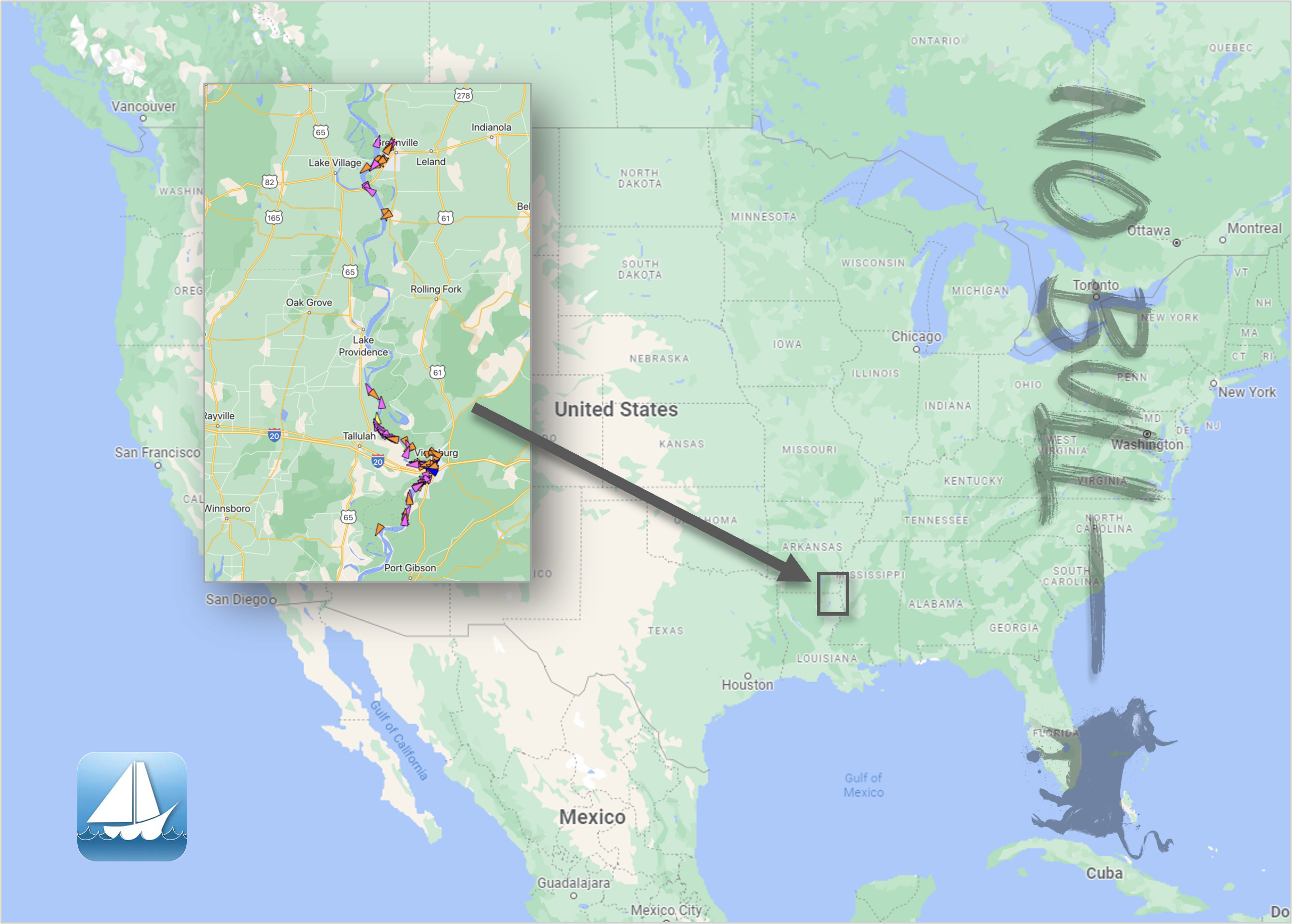

The Mighty Miss: She’s LOW and heading lower

Not sure if you heard, but the Mississippi River is quite low.

This is in Greenville, Mississippi. Can you imagine trying to maneuver a quarter-mile-long tow through that?

The Lower Mississippi has been dealing with groundings (aka ‘she’s stuck’) resulting in intermittent closures for the past three weeks.

The logjam has ensued with two problem spots: issues near Memphis and larger, industry-rattling disruptions at Lake Providence, Louisiana.

How bad it is?

Earlier today, my pal Michael Hirtzer and crew at Bloomberg reported a closure in the area resulting in a backup of 117 vessels and 2,048 barges.

Likewise this afternoon, American Commercial Barge Line reported a queue (boats waiting to pass) of 80 northbound and 60 southbound vessels.

According to ACBL, the Army Corps of Engineers will survey the channel tomorrow morning and if the all-clear is given, northbound traffic will run for 24 hours followed by 12 hours of southbound.

The River will then be closed for 36 hours afterward for additional dredging.

They call it a nightmare, Brian. A nightmare.

This game of red light, green light couldn’t come at a worse time for U.S. producers, grain companies, and anyone involved in river transportation as October and November are the busiest months for U.S. grain exports.

I want to show corn + soybean exports two different ways because 1. these are hard on the eyes and 2. it is important to visualize both what time of year we see the largest total volumes and the clear contrasting seasonality of the two.

No doubt about it - October and November are IMPORTANT. In fact, they are CRITICAL to say the least.

Now - the seasonality.

Soybeans dominate the fall into early winter months, while corn takes charge after the first of the year.

Wonder why soybean bids often tail off after January?

This is why!

We lose our edge as the world prepares to buy cheap Brazilian new crop bushels in late Feb/early March.

Speaking of losing our edge… or perhaps, falling off of a cliff - check out nearby soybean basis in St. Louis:

That cracking sound you heard was basis falling from an all-time high just a few weeks ago to a nasty low of more than $1 under SX for October delivery.

If you’re wondering - it is NOT because exporters do not want the soybeans. In fact, the opposite is true as October CIF continues to set the world on fire:

Here is the culprit:

Nearby freight is now offered at 3500% of tariff. In other words if you’re in St. Louis and you need a barge, you’ll have to shell out the equivalent of $4.19/bushel of soybeans.

Enough said.

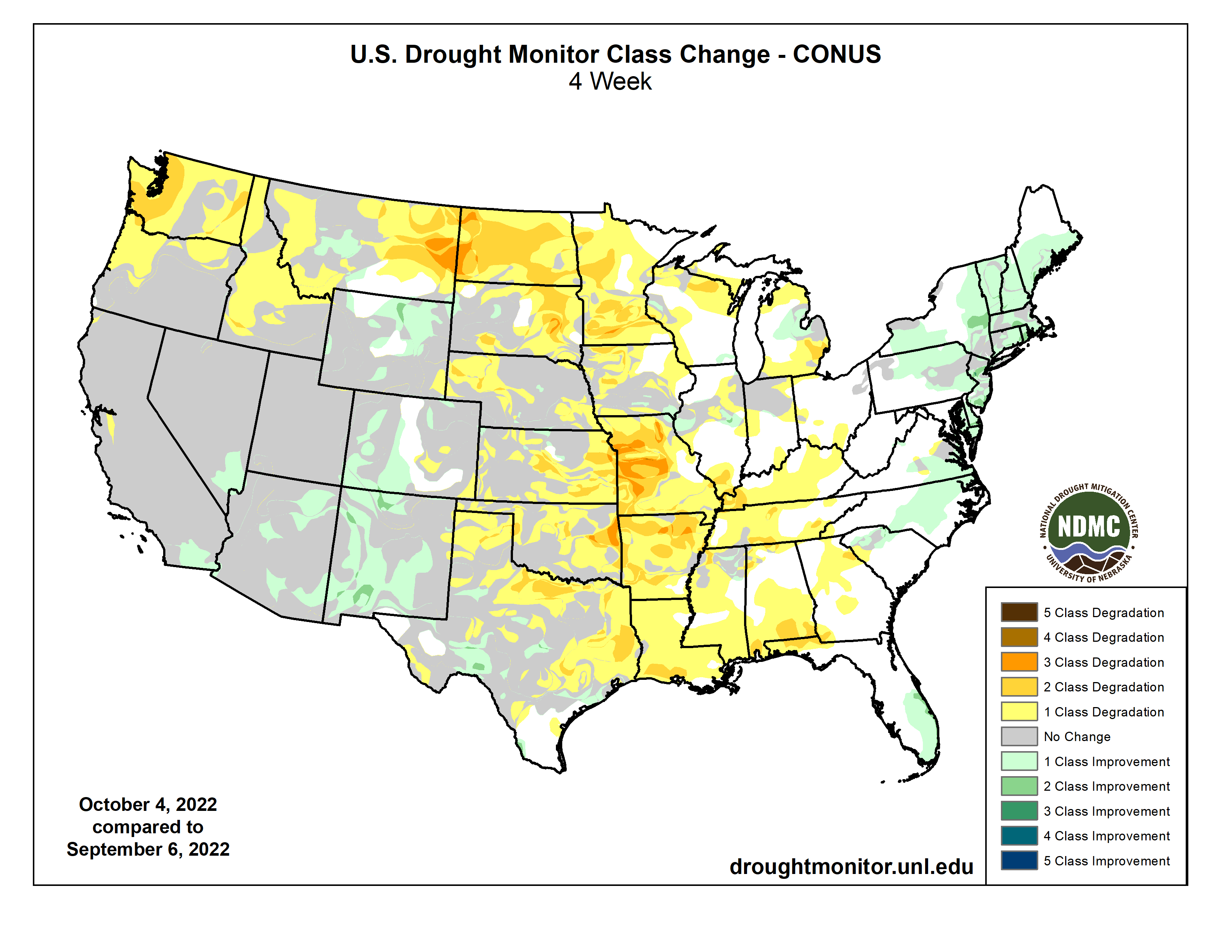

How did we get this low?

I guess since the growing season is over with I have been slacking paying much attention to the Drought Monitor. Turns out, it has grown significantly worse in recent weeks:

Check out these changes…

Taking a closer look at the Mississippi - no wonder we are on the struggle bus:

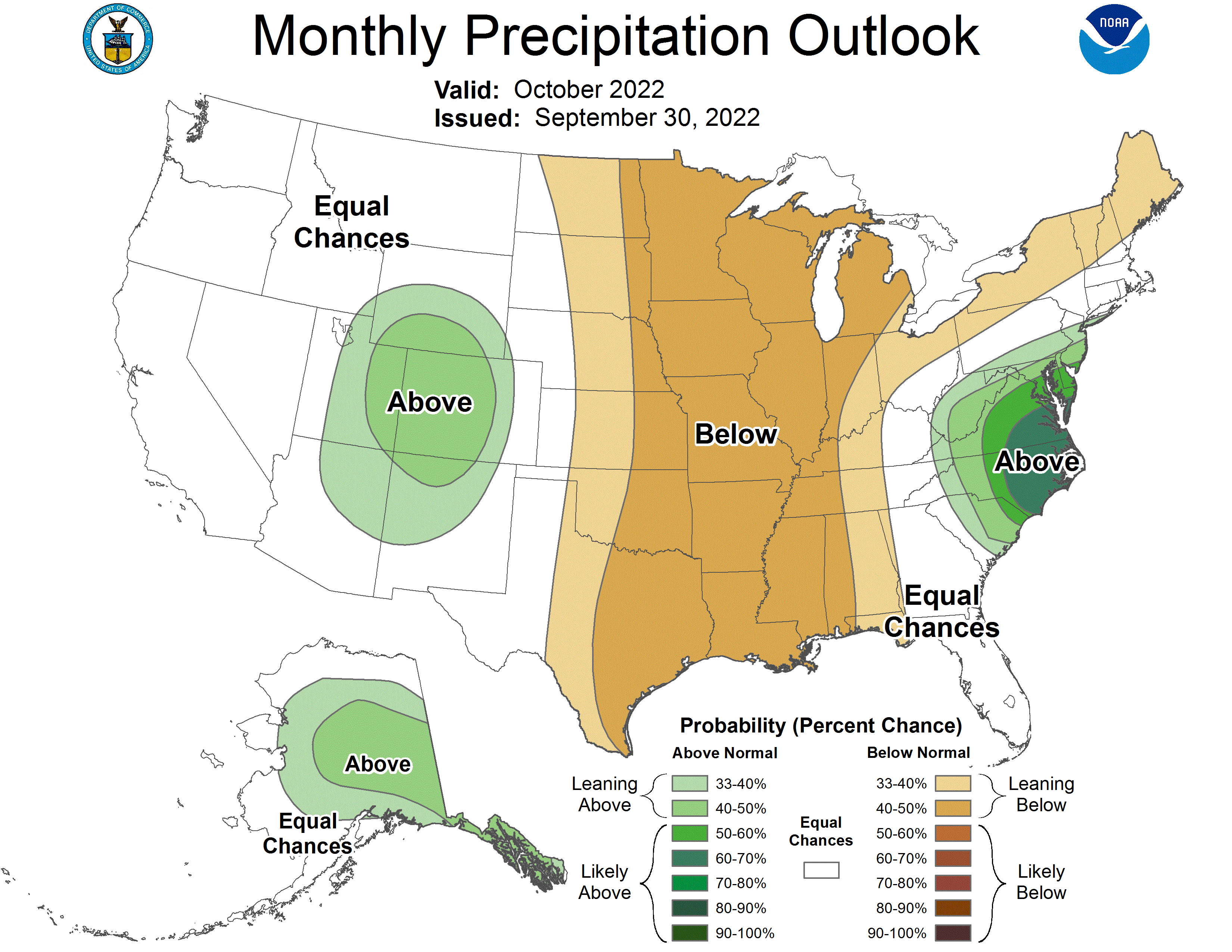

Even scarier (as far as the river is concerned) is the lack of significant precipitation on the way:

5-Day Cumulative Precipitation Forecast

7-Day Cumulative Precipitation Forecast (these are notoriously inaccurate, but hey we will take whatever we can get although doubtful a 1/4 of rain helps much)

No need to visit a haunted house this year… the October outlook is quite frightening, with a gigantic trough of below normal precip centered right atop the Mississippi…

The bottom line: this problem isn’t going away anytime soon.

Final Thoughts

How low can you go?

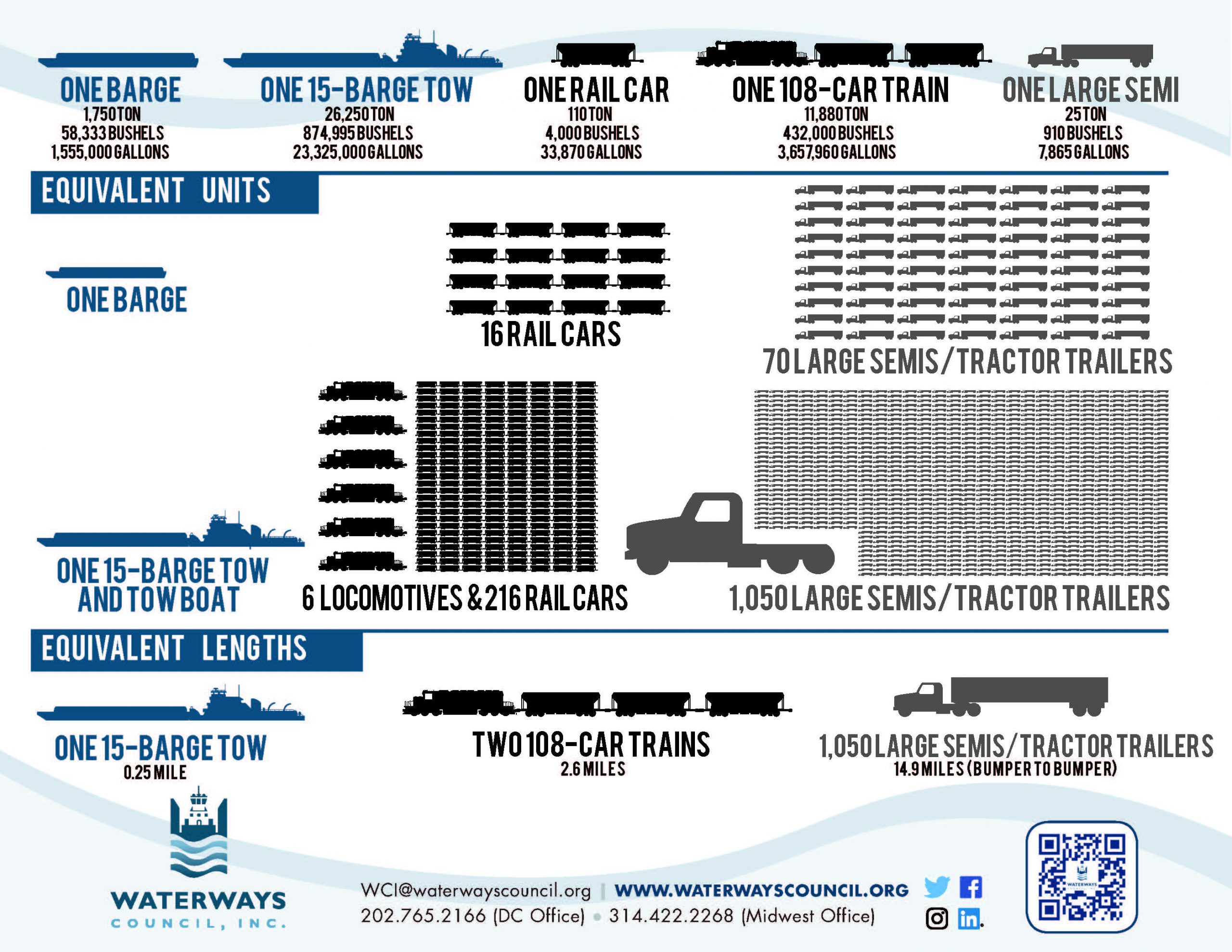

This is one of my all-time favorites:

Remember, barges vary in size and obviously capacity/tow sizes vary with river conditions, but you get the point.

I didn’t get into the details this evening, but this mess will have a long tail. Gulf exports will be handicapped until we see river logistics improve.

Now, does this mean freight will trade or stay at 3000%?

No. It makes zero sense for freight to trade at 3500%. Plus, if you are hauling to the river at -$1, we need to have a talk.

Here are a few take-home pointers:

If you have space, use it.

The carry does you no good until you lock it in

Corn export sales were horrendous this week

Export inspections will be eye-popping for all the wrong reasons in the coming weeks

Oct WASDE is Wednesday. We adopt USDA’s new 21/22 end stocks as new crop carry-in, plus see changes to yield… and eeekkkk demand (although USDA is likely to slow play what’s happening on the Mighty Miss for now)

Oh yeah, there is still a war going on in Ukraine

Alright, that is all for this evening.

Thank you SO much for being a loyal (free) subscriber for a couple years now. The real fun starts next week.