In case you missed it, NO BULL---- Out with the old, in with the new

New to NO BULL----?

It's fantastic and better yet, it's FREE

CLICK HERE TO BE ADDED TO THE LIST

09/01/2022

Out with the old, in with the new

Nothing new with Tripp... spending his weekends hauling hay for "fun".

Yep - that's him. The third-grader who can back a tractor more precisely than most grown men.

New House = New, Larger Price Tag

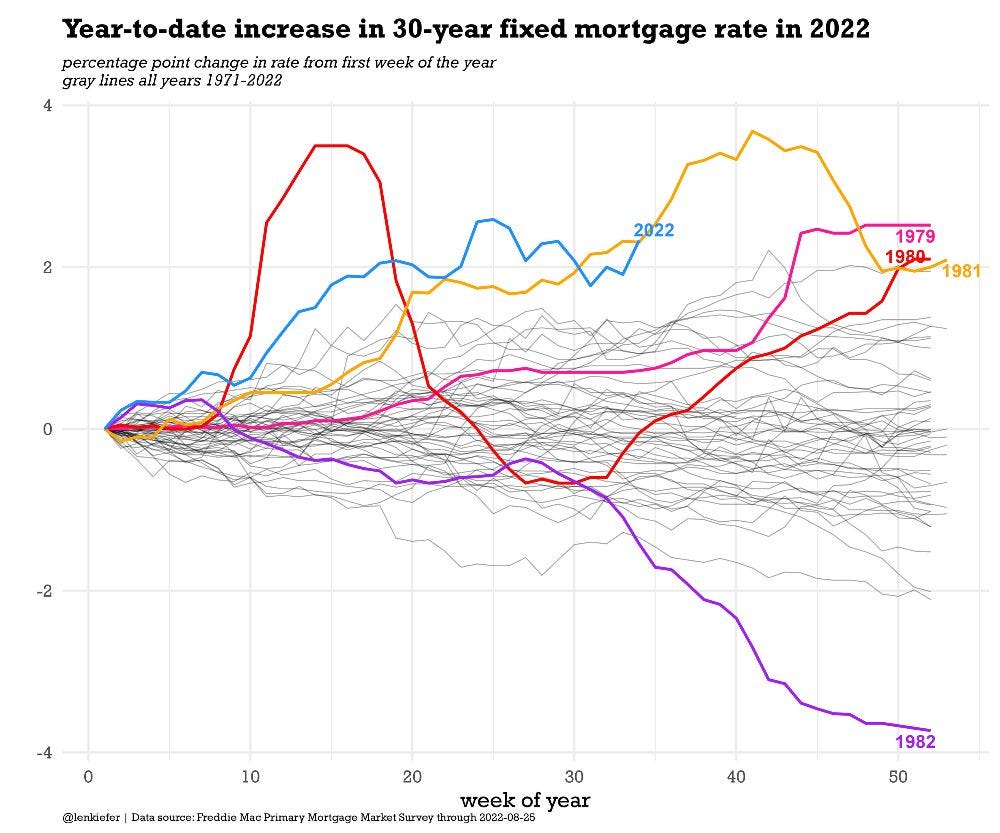

Whoa baby, this trend is not your friend.

Not only are higher prices making homes less affordable, but rising rates are putting the whammy on affordability as noted by the Federal Reserve Bank of Atlanta below:

The U.S. 30-year fixed-rate mortgage averaged 5.66% as of September 1 - double its rate one year ago and moving at a breakneck pace so far in 2022:

And finally, let's put today's rates in perspective:

Old Dirt, New Owner

Iowa has done it again, this time as an 80 went for.... brace yourself...

...$26,000 an acre earlier this week.

According to Jim @theLandTalker Rothermich, this is a new record-high price for pure agricultural land in the state. $2,080,000 for that parcel, while the second tract ~151.59 acres~ sold for $20,100 an acre.

Iowa always seems to win the prize for attention-grabbing price tags, but this Indiana auction is just as noteworthy:

A few weeks ago, 1,120 acres in Indiana, just south of I-70 near the Ohio border, sold at auction. Lawton Farms consisted of 13 tracts of some of the best soils in the state, located within close proximity of each other.

The large amount of contiguous land brought the crowd out in force as 76 registered bidders battled it out for two hours over the 13 tracts. The highest-priced tract went for $19,545 an acre.

By the time the auction was over, ONE bidder walked away with all 13 tracts for a total of $18.6 million. According to reports, the buyer (from Indiana) already owns several farms in that same area - now scooping up another 1,112 acres at an average of $16,556 each.

One (marketing) year ends and another begins

Yesterday marked the close of the 2021/22 marketing year, while today marks the beginning of 2022/23, which runs from September 1, 2022 through August 31, 2023.

Even though a the marketing year for corn and soybeans runs the 12 months from September to August, we get to endure 18 USDA reports with updated supply and demand estimates over the lifespan of the 2022 crop.

Initial (new crop) projections are made in May and then followed by monthly adjustments throughout the summer and into the fall. Production estimates are set in stone in the January report (cough cough, nothing with USDA is ever set in stone) but demand remains a moving target until the dust settles after September 1 stocks are released on September 30 and final numbers for the prior marketing year are reported on the October WASDE.

It is always interesting to look at ending stocks estimates by crop year over the course of USDA's 18 WASDE updates.

For corn, the 2020 crop year was the most notable by far as we slid from a record 3.3 billion to bare-bones stocks at year-end. Since then, we have been bare-bones as sub-1.5 billion has become the norm.

Soybeans... what a roller coaster. This one makes my chest hurt just thinking about it!

New Demand

Congratulations to my friends at Consolidated Grain and Barge on last week's ground breaking of their new soybean crushing facility in Casselton, North Dakota.

The plant ~North Dakota Soybean Processors~ is a joint venture between CGB Enterprises and Minnesota Soybean Processors. The facility will crush more than 42.5 million bushels of soybeans annually and should be in operation by 2024. You can read more about the groundbreaking HERE.

Does it seem like there are all kinds of new soybean crush plants being announced? That is because there are.

In fact, there have been announcements for new builds or expansions that total 630 million bushels of added crush capacity by the year 2026.

It is like the Ethanol Boom 2.0 as the push for all things green has lit a fire under renewable diesel. California's Low Carbon Fuel Standard (LCFS) jumpstarted the revolution, providing significant incentives and support for renewable diesel (intended to be made from waste fats/oils, but the margins are big enough that soybean oil has quickly turned into the feedstock of choice for production).

Soybean oil has spent decades as the ugly red-headed stepchild of soybean crush. Crushing beans yields meal and oil, with meal being the only product with real value (as a protein-rich feed ingredient) - until now. Soybean oil is no longer a pain in the backside for crushers - it has value of its own and big, fat margins abound.

As a result, everyone wants on board - from grain companies to traditional soybean processors and even Big Oil. In fact, Big Oil learned their lesson with ethanol. If you can't beat 'em, join 'em, teaming up with soybean processors to ride the wave.

This EIA graph is from 2021 so it likely missing some of the more recent announcements, but you get the point. Thank you, California for spurring a biofuel revolution.

As one would expect, when you add crush capacity or build a new plant - you intend to use it. For that reason, crush continues to set new records. US 2021/22 crush was forecasted at a record 2.205 billion bushels in the August report, while 2022/23 crush is expected to be another new record at 2.245 billion.

Crush and exports make up ~97% of US soybean demand with both inching closer towards an even share in recent years. Exports have increased as China's insatiable appetite for soybeans has grown and crush's share has been sliding since accounting for 65% of total demand back in the nineties.

More recently, crush did the heavy lifting during the Trade War of 2018 and 2019 - topping out at 55% of demand in 2019/20 before settling into a spot on par or marginally higher than export volumes.

As new crush facilities come online, it is obvious we will see an even larger demand-pull that ultimately keeps bushels away from export channels.

If I was one of your typical media-types looking for an extra dramatic story, I would do the math backing into how many additional acres of soybeans we will need to plant here in the US to satisfy all of this new crush capacity demand... I will spare you the line of bull----, however.

Supply and demand is the ultimate ebb and flow. It's never a one-for-one tradeoff. We won't add millions of acres instantaneously just like we won't see US soybean exports come to a screeching halt.

The landscape is changing though. Consider North Dakota for instance, where ADM is building a facility (joint venture with Marathon) that will crush 150,000 bushels of soybeans each day. Head 60 miles east and you'll run into CGB's (North Dakota Soybean Processors) plant that will chew through another 125,000 bushels a day.

Add those two plants together and you have nearly 100 million bushels in new annual crush capacity within an hour's drive when the entire state of North Dakota is not even projected to produce 200 million bushels of soybeans in 2022.

Granted CGB's NDSP plant sits in one of the top 5 soybean producing counties in the country (Cass, ND) - this crush capacity explosion will have a ripple effect.

Here is an example - CGB's North Dakota plans hit a snag when the local ethanol plant protested the venture. The CORN ethanol plant was opposed to the SOYBEAN crush plant because they argued it would ultimately drive up the price for corn in the area. Read more HERE.

Spoiler alert - Tharaldson Ethanol did not get their way...

FINAL THOUGHTS

Out with the old, in with the new

One of the biggest mistakes I see producers make time and time again is not adapting when things change.

The only constant in life is change, so you better get used to it.

There millions of things that are changing...

From the way you farm, to inputs, tractors, technology, and so on. The list is endless.

The way we receive information is changing too. Remember faxed bid sheets every afternoon? Or calls to the elevator asking for a bid?

Websites and apps have quickly replaced old ways of communication just as crude oil, currencies and geopolitics have replaced some of the more traditional market drivers.

And speaking of market - it is a global one and it is not coming back (to the US).

Brazil is set to out-produce the US on soybeans by more than 1 billion bushels this year.

I am confident I just offended a few die-hards in the I-states, but at some point we have to face the facts.

Out with the (old way of thinking) and in with the new.

Markets are moving forward with or without you. The sooner you hop aboard the education train and embrace the changes we are living, the better prepared you will be for the road that lies ahead.

PS - The map that I made at 6am detailing US crush capacity expansions is already outdated. There was another new plant announced mid-morning in North Platte, Nebraska - located along I-80, nearly to the panhandle. This would be the most western of any recent plant announcements with capacity to crush 110,000 bushels per day for a total of more than 36 million a year. Check it out HERE.